The trendiest type of home equity line of credit is in the crosshairs of Canada’s banking regulator, which is looking to curb risky borrowing as rising interest rates put added pressure on heavily indebted homeowners.

The product under scrutiny is the readvanceable mortgage – a traditional mortgage combined with a line of credit that increases in size as a customer pays down the mortgage principal. The regulator, the Office of the Superintendent of Financial Institutions (OSFI), calls them combined mortgage-HELOC loan programs, or “CLPs,” and has been watching warily as they have exploded in popularity while home prices have soared.

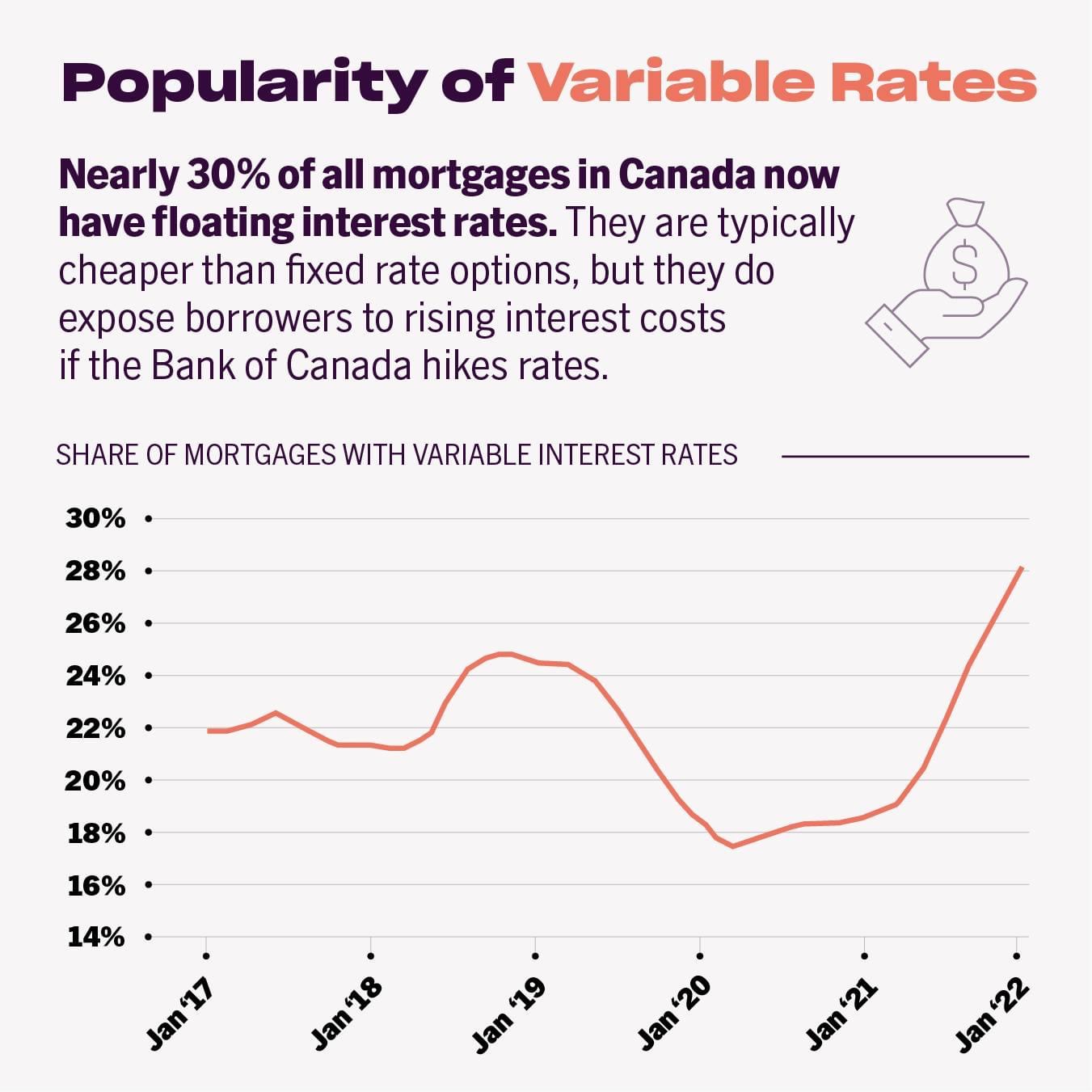

In the first two years of the COVID-19 pandemic, readvanceable mortgage borrowing increased 34 per cent and the combined-loan products had a total value of $737-billion in the first quarter of 2022, according to Bank of Canada data. That accounted for 42 per cent of all residential secured lending, higher than 37 per cent in the first quarter of 2020 and 36.5 per cent in the same period in 2019.

Now more than ever, owning a house is not a retirement plan

What mortgage rate should you choose right now? Three economists weigh in:

That sharp increase has caught OSFI’s attention. In a January speech, Superintendent Peter Routledge said readvanceable mortgages now make up “a significant portion of uninsured Canadian household mortgage debt.” And while he acknowledged they can be useful financial tools when used responsibly, Mr. Routledge said “they can also create vulnerabilities” for the financial system and increase the “risk of loss to lenders.”

OSFI has said it will announce changes to the rules governing these products this spring, and outlined two key concerns. One is that the ability to borrow back equity from a home after each principal payment has the potential to keep customers deep in debt.

The other is that HELOCs can be used to mask cash flow issues a borrower may have, making it harder for lenders and regulators to detect looming problems, especially in times of crisis.

In a speech last November, Mr. Routledge hinted OSFI might compel banks to classify readvanceable mortgages as loans that are more risky, which would make them more expensive for lenders to carry on their books as they would have to set aside more capital against each loan. He also said the regulator may tighten up the rules about how lenders underwrite these loans.

Bankers and mortgage industry experts say the regulator could also rein in limits on how much homeowners can borrow against their homes, or force them to requalify for increases to their HELOC.

Those changes might help curb some of the most precarious borrowing, but it isn’t clear they would significantly slow the demand. Experts say banks would likely pass on higher capital costs of those mortgages by charging customers higher interest rates.

“It would raise the costs for the lenders, in which case the pricing strategy for those types of products would have to be recalculated for all lenders,” said Maxime Stencer, a director with mortgage lobby group Mortgage Professionals Canada. “If there’s more costs involved in manufacturing that product and holding that product, then it becomes more costly to provide it to the customers, so customers would probably be affected by it.”

Readvanceable mortgages are now a staple product for most major lenders. Banks pitch them as a powerful borrowing tool that allows customers easy access to the equity in their homes.

A website promoting Bank of Montreal’s Homeowner ReadiLine puts the concept of the readvanceable mortgage succinctly: “Apply once. Borrow some. Pay back some. Borrow again. Pay down your mortgage. Borrow even more.”

Other banks have branded their readvancable mortgages with punchy names such as TD’s Home Equity FlexLine and CIBC’s Home Power Plan. Spokespeople for Canada’s five largest banks declined to say what proportion of their overall mortgage lending these products represent.

But regulators say the products also risk allowing customers to spend beyond their means and accumulate persistent debt that can make them more vulnerable in an economic downturn.

As national home prices skyrocketed late last year, Mr. Routledge said in November that the ability readvanceable mortgages give homeowners to boost their borrowing “may be simultaneously fuelling and helping Canadians afford rising home valuations.” That is because homeowners can borrow on lines of credit tied to their existing homes to buy vacation and investment properties.

Today, the housing market has cooled dramatically owing to higher mortgage rates. Economists predict the typical home price in Canada could decline by double-digit percentages this year.

That would lower the value of a homeowner’s property relative to the size of their mortgage and push them closer to a level of debt that OSFI views as troublesome: Borrowers who owe their lender more than 65 per cent of the value of the home, also known as a loan-to-value (LTV) ratio, which is a key metric used to assess risk in the financial system. A higher ratio represents a high level of indebtedness that could pose more problems for the financial system.

“That subset of borrowers who owe more than 65 per cent LTV poses the greatest risk,” said OSFI spokesperson Carole Saindon in an e-mail this week.

According to Bank of Canada data, borrowers above that threshold represented 28 per cent of the outstanding combined mortgage loans in the first quarter of this year. In the first quarter of 2020, the percentage was 42 per cent.

It is not clear whether that higher-risk borrowing level declined because home prices are up significantly, or because borrowers were drawing smaller amounts from their HELOCs.

Regardless, with home prices starting to cascade down, the lower prices will put upward pressure on homeowners’ LTV ratios.

“It is critical to note that these figures are calculated on the current market value of the homes and are subject to change as the market moves,” Ms. Saindon said. “If housing prices pull back from those peak levels, we would expect current LTVs to increase and the portion above 65 per cent to increase as well.”

That means borrowers could suddenly find themselves with a much higher ratio. If they breach the 65 per cent LTV threshold on the HELOC portion of their combined loan, they will have to start paying down some of the HELOC principal. For borrowers who are stretched to the max, this could wreak havoc on their finances.

Most HELOCs only require customers to pay the accrued interest, not the loan’s principal. And because the loans are secured against a borrower’s home, they typically carry lower interest rates than unsecured debt.

One reason banks like offering readvanceable mortgages is that they make consumers less likely to switch to a competitor. It is easy to assign a traditional mortgage from one bank to another, but a CLP must be fully discharged from one lender and re-registered with the new one. That process requires the borrower to pay fees and go through administrative hassles.

It is unclear whether these combined loans pose an imminent risk to the financial system. Bank of Canada data show that a large proportion of customers have relatively low levels of debt. As of the first quarter of this year, 41 per cent of combined loan borrowers had an LTV at or under 50 per cent.

The mortgage industry says OSFI is overreacting. They say HELOCs give borrowers easy access to the equity in their homes at a lower interest rate than other loans such as credit cards, personal lines of credit and payday loans.

HELOCs are commonly used for home renovations, investments in rental properties, to consolidate more costly debt from credit cards at lower interest rates, as well as a source of emergency funds if a borrower needs a quick cash infusion.

For example, if a borrower loses their job and no longer has employment income to pay their mortgage, drawing on a HELOC could be a low-cost, stopgap measure to make their mortgage payments while they look for another source of income.

“HELOCs prevent a lot more defaults than they cause. The reason is simple. When times get tough and you have no fallback liquidity, readvanceable mortgages let you continue paying your mortgage,” said Robert McLister, mortgage broker and strategist.

What worries regulators is when stopgap measures turn into permanent solutions – a cycle of borrowing that the Financial Consumer Agency of Canada has labelled a “home equity extraction debt spiral.”

(This article is from the Globe and Mail)

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages.

In August of 2020, at the young age of 37, Angela surpassed $1 Billion dollars in funded personal mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.