Recently, Angela was invited onto the Stress Test, a podcast hosted by the Globe and Mail, to answer some questions about everything one would need to know about mortgages in the current market. Here is what she said:

Pre-approvals, why do I need one and at what point should I get it?

“They’re critical. If you are thinking of buying a home in the next five years, you need to start thinking about your pre-approval now because you need to understand, based on today, ‘Where my income is? And where my credit is? What plan am I going to put in place to ever buy a home? How much income do I need to show?’ As an example, in today’s market, $100,000 in provable income qualifies you for a $400,000 mortgage. So, what does that mean for you? What type of property does that look at? What type of down payment do you have? How are you getting a down payment? Financial planning is critical, and you can’t create a plan without a map. The biggest mistake people make is, that as soon as they get a job they buy a car. Well, if they have an $800 per month payment, that takes away $200,000 in mortgage qualification. So, if homeownership is one of your goals, then way before you even think you’re going to need it. You need to understand your income, debt, and how you can save for a down payment to plug every dollar in the best possible place to get you a return. Not only on your taxable income but in every single way to ensure that you are setting yourself up for success. Because this isn’t something you just think ‘Okay I need to move next month, I need to go get a pre-approval. It’s a plan, so you need to start way before you think you do. So you can set up a plan to make sure you’re plugging your money in the best places.”

Tell us a little more about getting a rate hold. How long can I get a rate held for? We see rates rising almost week by week, month by month. How long can I lock in for?

“Some lenders will do up to 120 days, is average. Now again, with the variety of lenders that are out there. Some lenders that have the best rates, don’t do pre-approvals at all. Some lenders do pre-approvals for 120 days. Some 90 days. There is a cost to that. There is a why behind everything in the banking and mortgage and finance industry. When you think about that why, well it costs money for the lenders to hold money. Pre-approvals, only about 4 out of every 10 pre-approvals go live. So, for the banks to be holding money at a lower cost than they can lend out money at a higher cost or it no longer becomes available to them. There is a cost to that.”

Angela, how are the mortgage requirements different for self-employed workers or those in the gig economy? My understanding is that lenders like to see two years of consistent income.

“Correct, and again, it is about piecing it together. So if you’re in the same industry, maybe you have contracts with specific lenders. Well then, if we can piece it together and it makes sense and the story makes sense, and it’s the same type of industry but you just kind of shifted a little bit about how you get compensated, then there are lenders who have exceptions to that. So again, when you invest the time, and you invest in yourself, and see exactly what you need to do and where to go to get there. You’re going to have the clear picture, but you have to invest the time and it’s document-heavy.”

Let’s talk a little bit about interest rates, which are rising now. Buyers are subject to a stress test when they are getting a mortgage. For people who are applying for a mortgage, can you tell us how that works?

“Yes, you are tested for a mortgage on an, on average, 2% higher interest rate than what you are actually paying. So, that test is put there because it is anticipated that they want you to be able to qualify for the mortgage, should rates go up. On average, 2% from the time in which you got it. So knowing that that’s the plan that all the lenders have in place, all of us Canadians should be navigating our mortgage and financial plans for that. And then for whatever reason rates go down or they don’t go up as anticipated, you are the only winner because you have access to the equity in your home that you have protected yourself with in the event that things did change. You could do that in several different ways. You could either do that with your payment, or I recommend doing that on the side so that if you have an emergency come up you won’t have to go into debt outside mortgage at a higher rate to be able to navigate that. While it is important to look at your mortgage, you also have to consider how you plan your budget and navigate that to be able to have the most freedom in changing times.”

Angela, I’ve talked to mortgage brokers over the years and have continually been surprised by their stories of how many people break their mortgage before their renewal date. What happens if I break my mortgage?

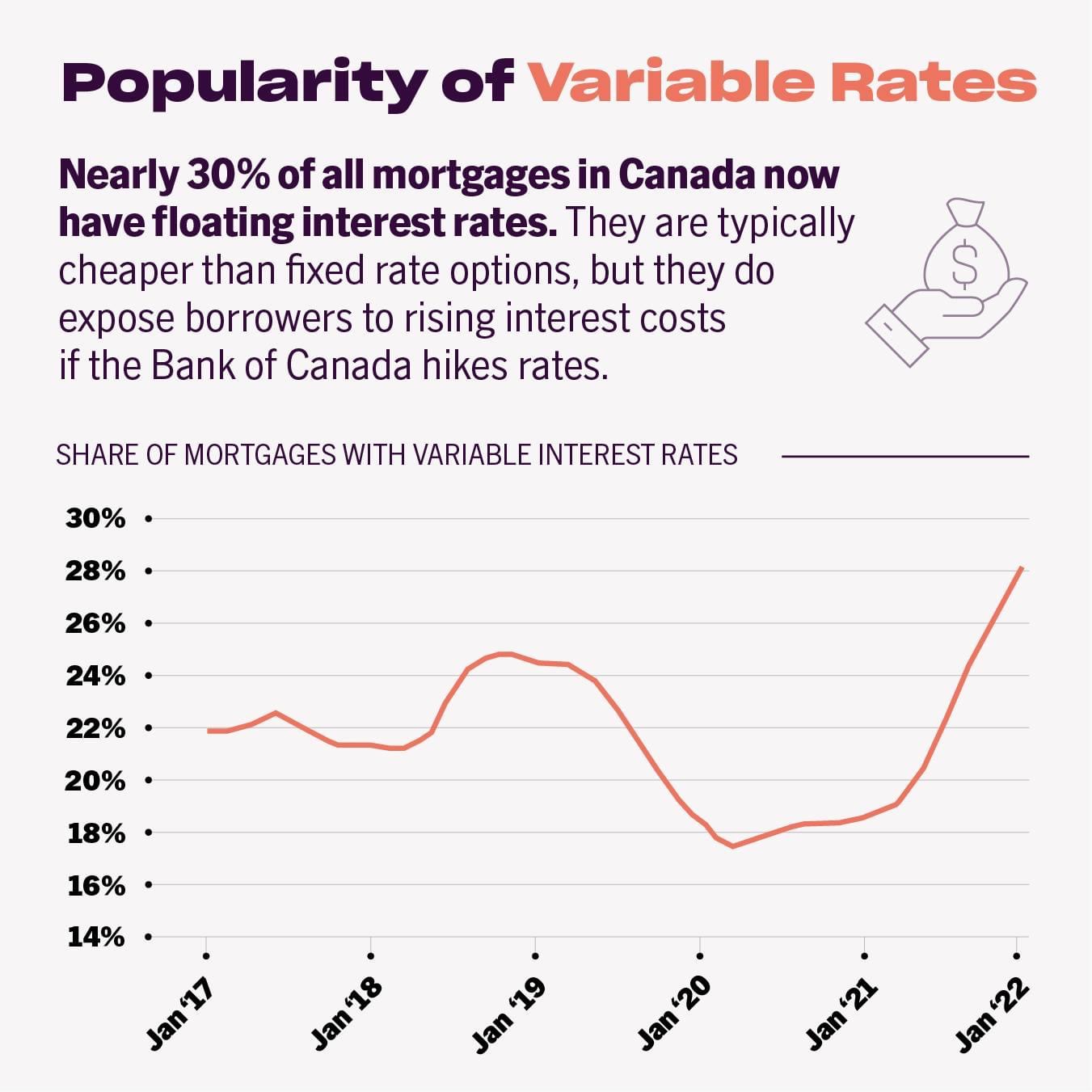

Seven out of ten, that’s why I recommend a variable as well. Because a variable is consistent, it always only ever has a three-month interest penalty. You know, we don’t know what’s going to happen with discounts. If rates go up, sometimes discounts go down. Maybe that’ll be the time when people can make their move because properties are not going to multiple offers anymore. So if you adapt a fixed-rate mortgage with a traditional bank, your penalty is going to be much higher; four or five percent to get out of. And that’s the thing, you can’t guarantee the timing of when you’re going to need something. That’s why seven out of ten Canadians end up breaking their mortgage early. So, are you going to be someone in that seven out of ten, or are we going to be lucky and not have any changes in circumstances? I know I like to set myself up for the most amount of success to control what I can. We can’t foresee the future, we don’t know if our relationships are guaranteed to last, and one person is not going to be safe forever. Am I going to change jobs? Am I going to be blessed with a pregnancy? You can’t guarantee all those things in life, we get a lot of curve balls. I like to set myself up to be as successful as possible, utilizing every option that’s out there.”

What is the ideal downpayment?

“There is no ideal down payment. It’s whatever you can afford to get into the market ASAP.”

If I have extra money and I want to pay down my mortgage, how does that work?

“Easy, you either just email or call your lender but don’t do that until you are sure you have six months of emergency expenses aside, and that you can’t plug that money into somewhere else to get a tax refund or more cash on hand. Make sure what you do is in your best interest and no one else’s. It’s a one-way street when you put money down on your mortgage.”

What happens when I’m a homeowner, I’m short on money and I need to miss a payment.

“That’s why you keep the money in your account for six months of emergency expenses! Some lenders have that in their policy, some don’t. You contact them, you work it out, and they’re going to take care of you. But different lenders are different, that’s why when we said gig economy, I know some lenders are terrible for the gig economy and some are really good at it and allow you to skip some payments. Especially if unions go on strike and so forth, so again interview the people you work with, and make sure they get your lifestyle and goals.”

How do you get financing if you’re teaming up to buy a house with a friend or sibling, instead of following the traditional path of going solo or with a partner?

“Very risky, you need to document it up the yin yang. I can tell you the good, the bad, the ugly. I’ve done it myself, and I wouldn’t do it again. I would do it with a spouse or no one at this point. But you got a lot to consider because not everyone is exactly who they are and is influenced by the same people in 5, 10, or 20 years. You can’t guarantee if you will or will not qualify later down the road. So, you need to have a real hard thought about if you really want to do that and what your outs are.”

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages.

In August of 2020, at the young age of 37, Angela surpassed $1 Billion dollars in funded personal mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.