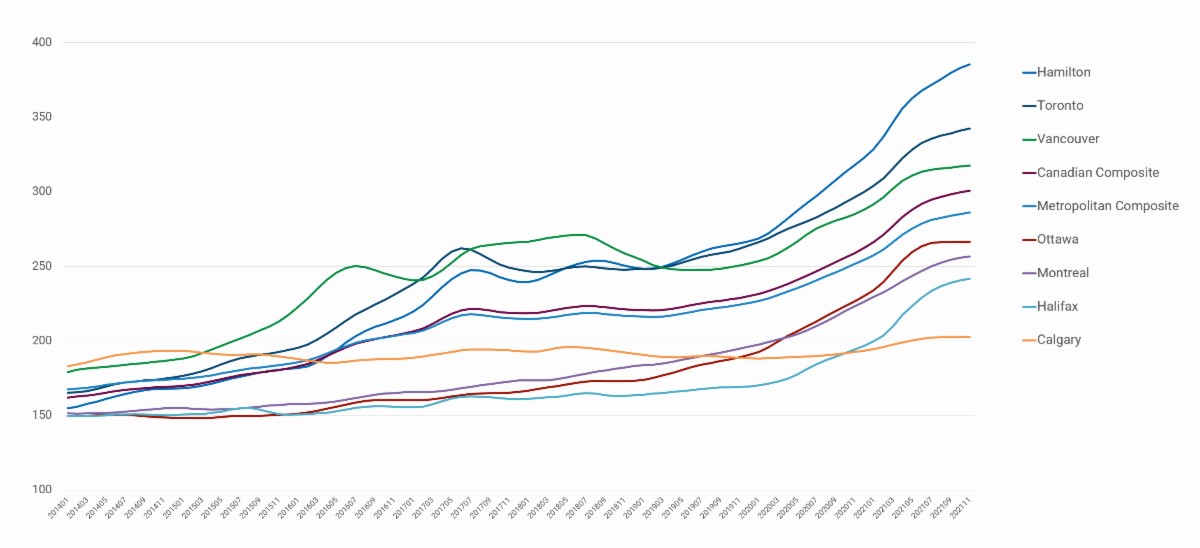

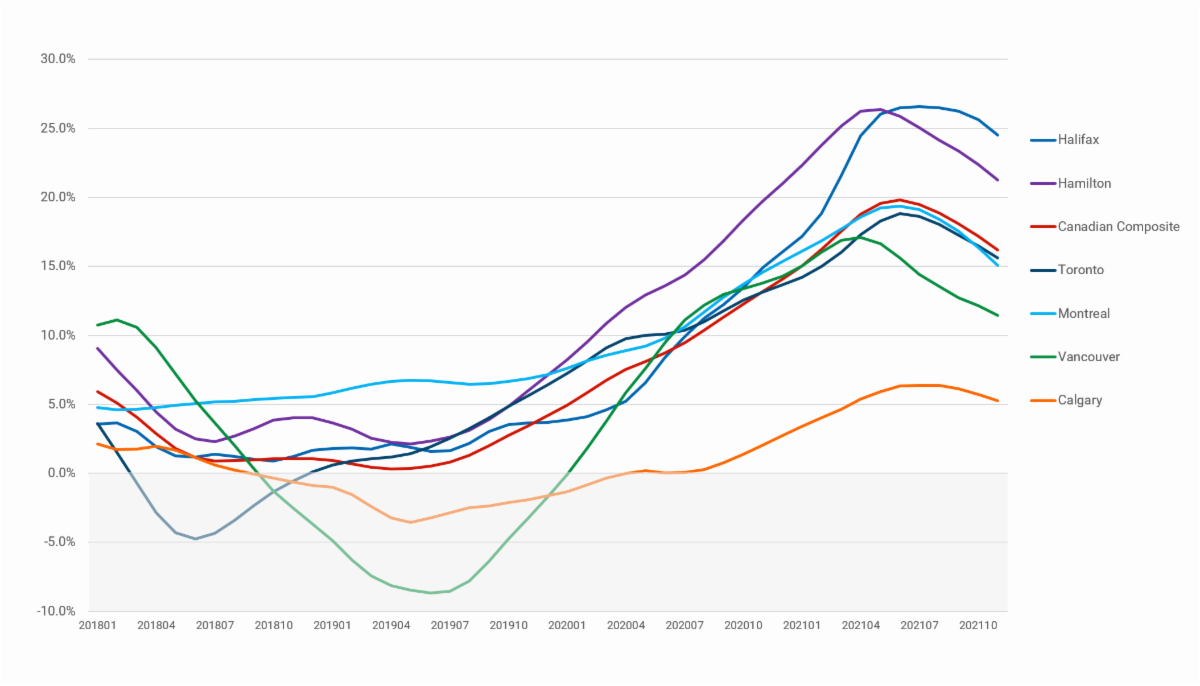

The Bank of Canada has made their announcement today to keep interest rates the same. However, it is likely that the rate will increase in the next announcement in March and most certainly this year overall. This is largely in part because of the lower economic activity during the pandemic, we are still below pre-pandemic numbers. As well, the Bank of Canada noted in their announcement in December that they would not be moving the rate until April. So, it is likely their plan to move up the timeline to increase the rates in March.

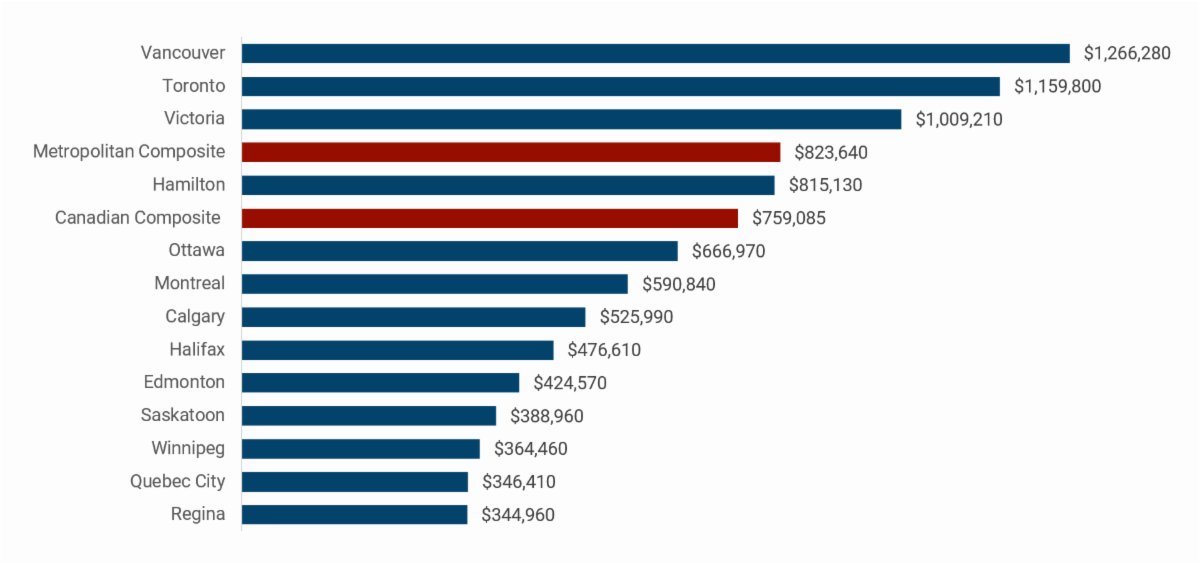

Even should the interest rate go up, variable-rate mortgages have become a much larger part of the overall housing market. Currently, the lowest variable rate is the prime rate minus 1.1%, which equates to a net rate of 1.35%! For reference, a $500,000 mortgage with a 25-year amortization period would equal $1964. While a comparable fixed-rate is 1.5% higher, equivalent to six increases of 0.25% from the Bank of Canada, which has been the standard amount, historically. The payment on this standard fixed-rate with the same mortgage would be $2328. That’s a $364 difference!

Of course, a variable-rate mortgage is not for everyone and is best suited for households that can afford a little fluctuation in their payments. But being able to do so will net you big positives in the future. The quicker you can pay down your mortgage the better a variable-rate will work for you. Because once we start chipping away at the highest point of the mortgage, the less material it ultimately becomes when interest rates go up in four or five years’ time.

With Canada’s latest inflation rate at 4.8%, and paying less than 1% on your mortgage rate, this is the closest we’ve ever been to free money! So if you or a loved one wants to take advantage of these historic low rates and use them to build your wealth, please don’t hesitate to reach out to us!

If you would like to see how different interest rates affect your mortgage payment, check out our DLC app for a free mortgage calculator!

Angela Calla is a 17-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages.

In August of 2020, at the young age of 37, Angela surpassed $1 Billion dollars in funded personal mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.