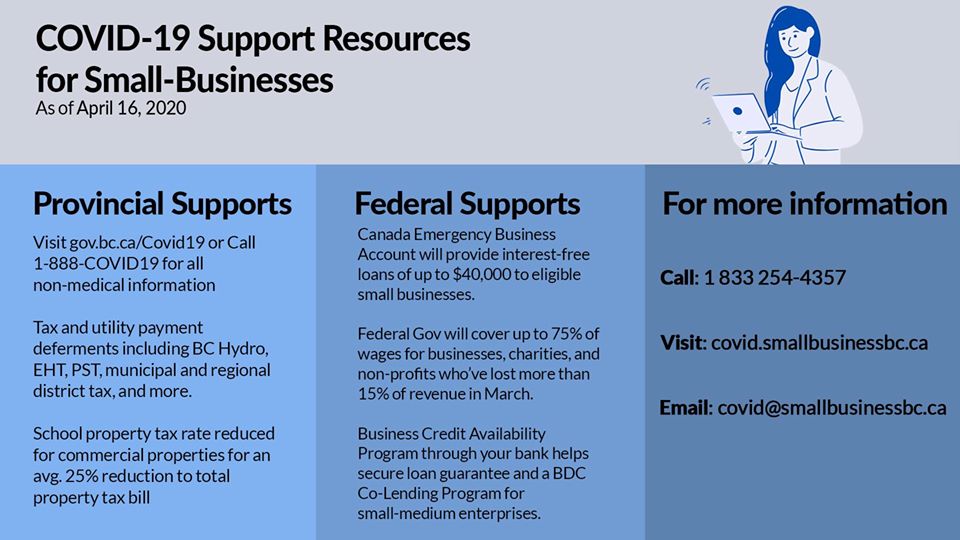

How You Can Access Online all your Interactions with your CRA and Service Canada Accounts Online, Anytime!

My Service Canada Account (MSCA) is a secure online portal that lets you apply, view and update your information for:

- Employment Insurance (EI)

- Canada Pension Plan (CPP)

- Old Age Security (OAS).

- And now also any of the many COVID-19 benefit programs for Canadians.

If you do not already have one, start by creating your Service Canada ‘My Service Canada Account’ here .

Within your ‘My Service Canada Account’ you should first setup or to confirm that your direct deposit account information is correct to facilitate the receipt to your bank account of any Government of Canada benefits, from CPP to OAS and EI and any of the many COVID-19 benefit programs.

To do this, login and go to ‘Service Canada account services’ and in the View/Change tab click on Canada Pension Plan (CPP) / Old Age Security (OAS) link and then click on ‘Payment information’ and then click on ‘2020’ and it will then display the payments you have received for both pensions by date.

Connecting your ‘My Service Canada Account’ with your CRA ‘My Account for Individuals’

From your My Service Canada Account, you can also securely access your income tax and other benefit information by clicking on the Canada Revenue Agency “My Account” button. This will connect you to your Canada Revenue Agency account without having to login or revalidate your identity. And if you have not yet registered for your online CRA ‘My Account for Individuals’ you can do this here Registration process to access the CRA login services

Learn how you can also sign in to your My Service Canada Account from your bank account login

My Service Canada Account: Register with your bank

Link between My Account and My Service Canada Account

The link provides you with a convenient connection between the Canada Revenue Agency’s (CRA) My Account for Individuals and Employment and Social Development Canada’s (ESDC) My Service Canada Account.

If you are registered for CRA’s ‘My Account for Individuals’ you can securely access ESDC’s My Service Canada Account without having to login or revalidate your identity. The link will take you directly to your My Service Canada Account within a single secure session, without having to sign in or register with MSCA.

Using the “Tell Us Once” feature you can now update and share your direct deposit banking information with both CRA and ESDC in one easy step.

Individuals receiving a Canada Pension Plan (CPP) benefit, will be able to update their banking information with one department and can choose to share it with the other. Canadians can choose to share direct deposit information through multiple service channels including:

How to get your CRA ‘statement of account’

Your Statement of Account is what you will need when applying for a mortgage in order to prove you have paid any money showing on your NOA as owing to CRA.

Login to your CRA ‘My Account’ and you will land on the ‘Overview’ page. In the Accounts and section of that page click on ‘View statement of account’ and then print that page or save it as a pdf file.

Angela Calla is a 16-year award-winning woman of influence mortgage expert. Alongside her team, passionately assisting mortgage holders get the best mortgage, and educating them on The Mortgage Show on CKNW for over a decade and through her best-selling book The Mortgage Code available on Amazon. To purchase the book click here: The Mortgage Code. Proceeds from all sales will be donated to Access Youth Outreach Services. Angela can be reached at callateam@dominionlending.ca or 604-802-3983.