The Bank of Canada announced its 6th rate hike of the year this morning in an attempt to reach its target inflation rate of 2%. Prime rate now sits at 5.95% for most banks.

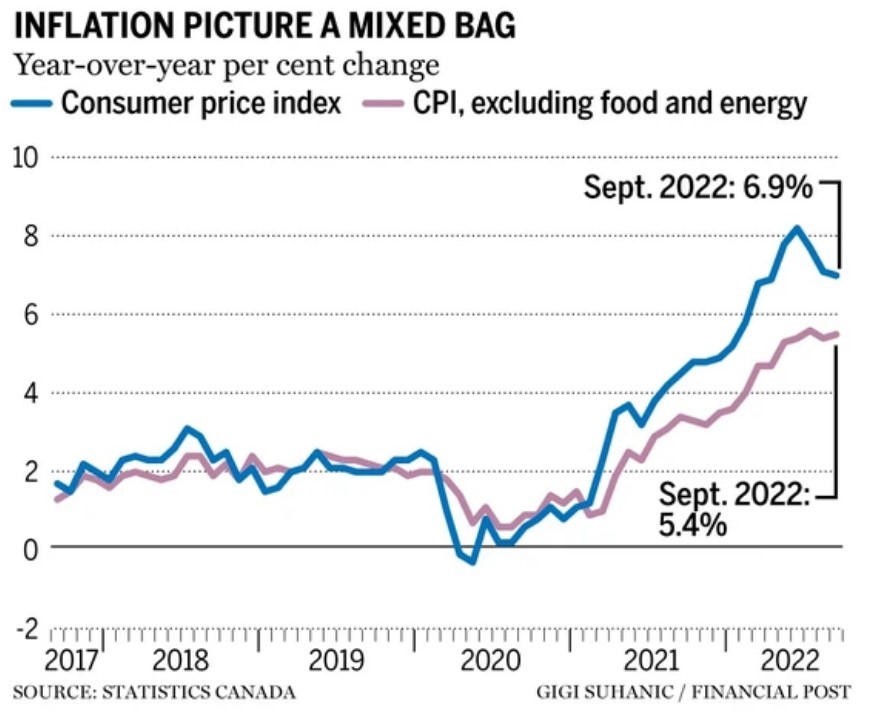

In September, the inflation rate was recorded as 6.9%, causing prices of food and other necessary costs to increase. The Bank of Canada states that by increasing interest rates, demand should slow relieving price pressures.

However, these hikes are causing some Canadian’s mortgage payments to increase by hundreds or even thousands of dollars causing protests to start across the country.

Fixed-rate mortgages are not affected by this specific change today as the bond market priced in this recent increase this past week. For new purchases or refinances, the qualifying rate has gone up decreasing the amount of mortgage home purchasers will qualify for moving forward.

With yet another increase of 0.50%, you can expect your monthly payments to increase by approx. $26 per $100,000 on most variable rate mortgages and/or lines of credit, with the exception if you have a fixed payment, then the amortization increases.

Watch the video below for a segment we did on Global News this morning.

Angela Calla also did a segment with CBC News for deeper information on this market change and trigger rates. Check out the video below.

Times are stressful, but we’re here to help guide you through these market changes and ease recovery. Get in touch with us at callateam@countoncalla.ca so our team can evaluate your financial situation and provide you with unbiased advice!

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

Bank of Canada Will Not Be Happy With This Inflation Report

Canada’s headline inflation rate ticked down slightly last month to 6.9%, but measures of core inflation remain stubbornly high, and food prices hit a 41-year high. Lower gasoline prices were primarily responsible for the decline in inflation in the past three months. Bond markets sold off on the immediate release of the data this morning, taking the 2-year yield on Government of Canada bonds to over 4%. This is the last major data release before the Bank of Canada’s policy rate announcement next Wednesday, October 26, which puts the potential for a 75-bps hike back in play. At the very least, the Bank will take the overnight rate up 50 bps to 3.75%, but I wouldn’t rule out another 75-bps move. Judging from experience, we may see a nod in that direction by Governor Macklem before the Governing Council meets.

Excluding food and energy, prices rose 5.4% year-over-year (y/y) in September, following a gain of 5.3% in August. Prices for durable goods, such as furniture and passenger vehicles, grew faster in September compared with August. In September, the Mortgage Interest Cost Index continued to put upward pressure on the all-items CPI Canadians renewed or initiated mortgages at higher interest rates.

Monthly, the CPI rose 0.1% in September. On a seasonally adjusted monthly basis, the CPI was up 0.4%.

Average hourly wages rose 5.2% on a year-over-year basis in September, meaning that, on average, prices rose faster than wages. The gap in September was larger compared with August.

In September, prices for food purchased from stores (+11.4%) grew faster year-over-year since August 1981 (+11.9%). Prices for food purchased from stores have increased faster than the all-items CPI for ten consecutive months since December 2021.

Contributing to price increases for food and beverages were unfavourable weather, higher prices for essential inputs such as fertilizer and natural gas, and geopolitical instability stemming from Russia’s invasion of Ukraine.

Food price growth remained broad-based in September. On a year-over-year basis, Canadians paid more for meat (+7.6%), dairy products (+9.7%), bakery products (+14.8%), and fresh vegetables (+11.8%), among other food items.

Bottom Line

Price pressures might have peaked, but today’s data release will not be welcome news for the Bank of Canada. There is no evidence that core inflation is moderating despite the housing and consumer spending slowdown. The average of the Bank’s favourite measure of core inflation remains stuck at 5.3%. Combined with the Governor’s recent harsh rhetoric, the high probability that the Fed will hike rates 75 bps at the next Federal Open Market Committee Meeting and the weak Canadian dollar, there is no doubt the Bank will increase their overnight policy target to at least 3.75%, and could well go the full 75 bps to 4.0% next week. I would bet that they will not quit there, with further hikes to come in December and next year by central banks worldwide.

The Government of Canada yield curve is now steeply inverted, reflecting the widely held expectation that the economy is slowing. The prime rate will increase sharply next week, increasing variable mortgage rates again. Fixed mortgage rates will rise as well, but not by as much, continuing a pattern we’ve seen since March when the Bank of Canada began the current tightening cycle. We are unlikely to see a pivot to lower rates in the next year as inflation pressures remain very sticky.

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

There are many unusual aspects to the current housing correction, but fundamentally the most noteworthy is how orderly and non-chaotic it has been. Home sales have slowed, but so have new listings, so the price declines are more muted than we might have expected. This is not a housing collapse. It is a housing correction. We’ve seen little distressed selling, as most would-be sellers have lots of home equity and low mortgage rates–not anxious to buy new properties immediately. Moreover, with rents surging, most potential down-sizers aren’t keen to make that trade-off.

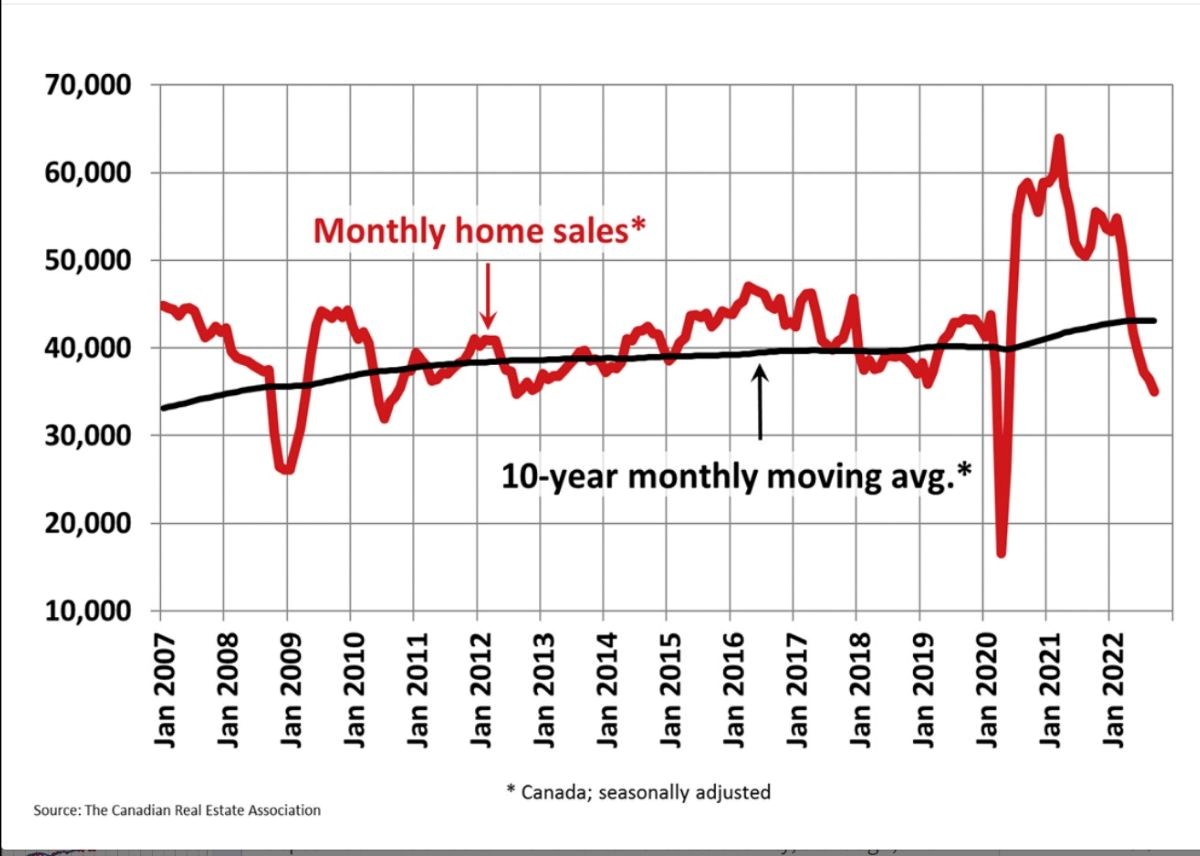

The full effects of the most recent rate hikes have not yet manifested. Statistics released today by the Canadian Real Estate Association (CREA) show that the slowdown that began in March in response to higher interest rates continued in September. Home sales recorded over Canadian MLS® Systems fell by 3.9% between August and September 2022. From May through August, month-over-month declines have been progressively smaller. The September result marked a slight increase in the current sales slowdown that began with the Bank of Canada’s first rate hike back in March.

While about 60% of all local markets saw sales fall from August to September, the national number was pulled lower by the fact markets with declines included Greater Vancouver, Calgary, the Greater Toronto Area (GTA) and Montreal.

The actual (not seasonally adjusted) number of transactions in September 2022 came in 32.2% below that same month last year. It stood about 12% below the pre-pandemic 10-year average for that month (see chart below)

“September was another month of lower sales activity, although, with many sellers also opting to play the waiting game, the market remains on the tighter side of balanced market territory,” said Jill Oudil, Chair of CREA. “It makes for an interesting dynamic, one that doesn’t really have many historical precedents. The market has changed so much in the last year, and the adjustment to higher borrowing costs is still underway.”

“Up until recently, higher borrowing costs had disproportionally affected the fixed-rate space, with buyers able to qualify more easily if they went with a variable rate mortgage,” said Shaun Cathcart, CREA’s Senior Economist. “The Bank of Canada’s most recent rate hike in early September finally closed that door, so it was not a big surprise to see additional softness on the sales side. The important thing to remember is we’re still in the middle of a period of rapid adjustment, with buyers and sellers trying to feel each other out while a lot of people have had to take their home search plans back to the drawing board. As such, resale markets may remain on the quiet side for some time yet, with the flipside of that coin being even more pressure on rental markets.”

New Listings

The supply of homes is still historically low. The number of newly listed homes edged back a further 0.8% on a month-over-month basis in September. This built on the 6.1% and 4.9% declines recorded in July and August, respectively, as some sellers appear content to stay on the sidelines until more buyers are ready to get back into the market. It was an even split between markets where new supply was down in September and those where it increased, with the most significant declines in the GTA offsetting the largest gains in British Columbia’s Lower Mainland.

Unusually, new listings would be so listless during a housing slowdown. However, the CREA data only go back 42 years, when interest rates trended sharply downward. Sellers today typically have mortgages at far lower than current rates, which no doubt dampens their enthusiasm to sell. Distressed sellers apparently listed their homes earlier this cycle, with the rest remaining on the sidelines for now. That could change if interest rates rise substantially further, although the incentives to stay in place continue high.

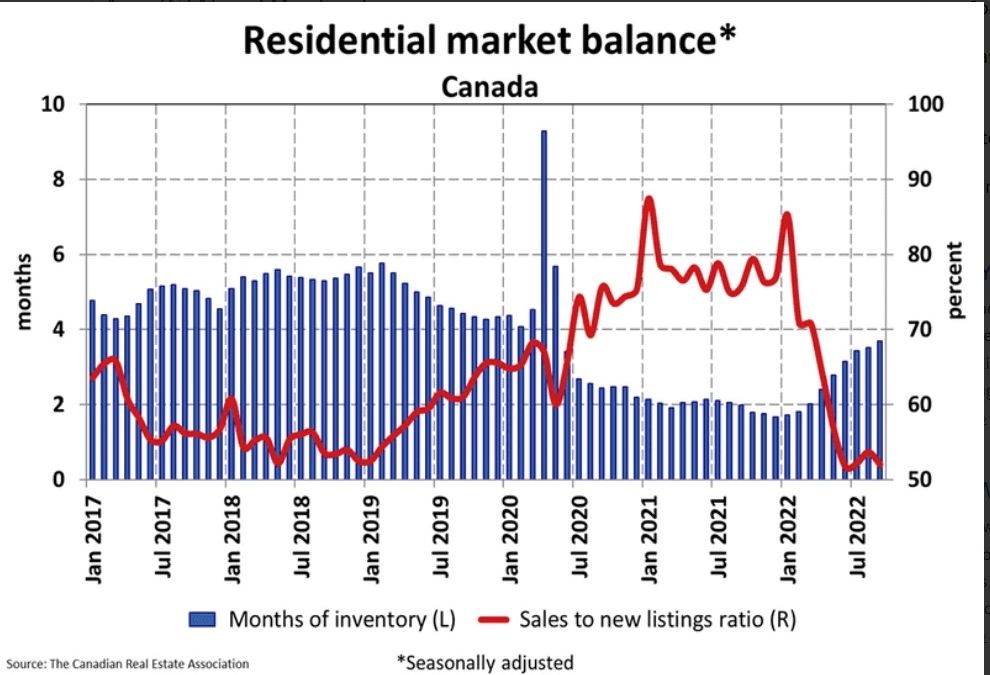

With sales down and new listings seeing a minor change in September, the sales-to-new listings ratio eased to 52% compared to 53.6% in August. The September 2022 reading for the national sales-to-new listings ratio was back on par with those in June and July and slightly below its long-term average of 55.1%.

There were 3.7 months of inventory on a national basis at the end of September 2022, up slightly from 3.5 months at the end of August. While the number of months of inventory is still well below the long-term average of about five months, it’s also up quite a bit from the all-time low of 1.7 months set at the beginning of 2022.

Home Prices

The Aggregate Composite MLS® Home Price Index (HPI) edged down 1.6% on a month-over-month basis in August 2022, not a small decline historically, but smaller than in June and July.

Breaking it down regionally, most of the monthly declines in recent months have been in markets across Ontario and, to a lesser extent, in British Columbia; however, in August, Ontario markets contributed most to the overall national decline.

Looking across the Prairies, prices in Alberta appear to have peaked. Prices still rise slightly in Saskatchewan, while Manitoba recorded the only decline. In Quebec, prices have dipped somewhat in the last couple of months. On the East coast, the softening of prices confined to Halifax-Dartmouth is now also appearing in New Brunswick, Newfoundland and Labrador. By contrast, prices in PEI continue to edge ahead on a month-over-month basis.

The non-seasonally adjusted Aggregate Composite MLS® HPI was still up by 7.1% on a year-over-year basis in August. This was the first single-digit increase in almost two years, as year-over-year comparisons have been winding down at a brisk pace from the near-30% record year-over-year gains logged just six months ago.

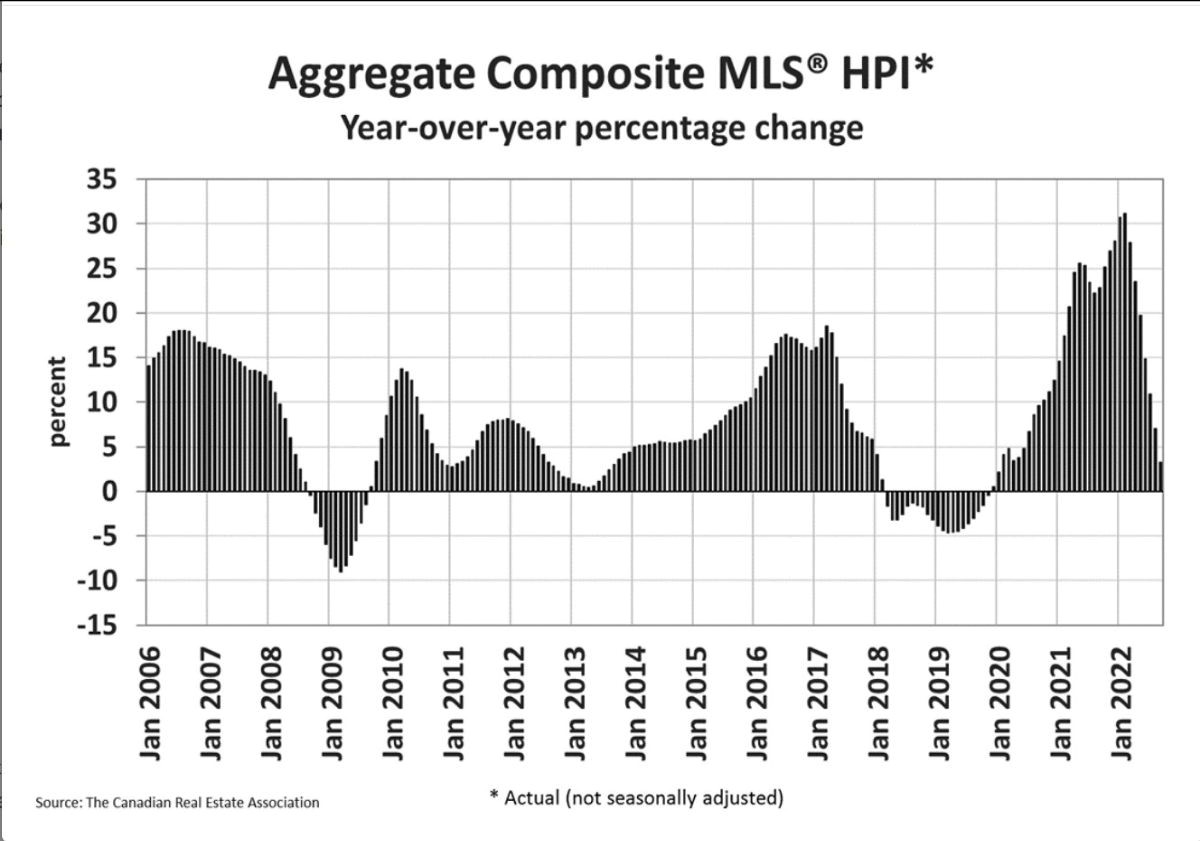

The Aggregate Composite MLS® HPI edged down 1.4% on a month-over-month basis in September 2022, not a small decline historically, but smaller than in June, July and August.

Breaking it down regionally, most of the recent monthly declines had been in markets across Ontario and, to a lesser extent, in B.C. The standout trend in August and September was that quite a few of those Ontario markets saw monthly price declines get stopped in their tracks, mainly in the Greater Golden Horseshoe. In a few markets prices even popped up a bit between August and September.

Looking across the Prairies, prices in Edmonton and Winnipeg are down a bit from their peaks, while prices are sliding sideways in Calgary, Regina, and Saskatoon. Similarly in Quebec, prices have dipped in Montreal but are mostly flat in Quebec City.

On the East Coast, price softness that had been confined to the Halifax-Dartmouth area appears to now be showing up in parts of New Brunswick and Newfoundland and Labrador, while prices in Prince Edward Island have flattened out in recent months but have not yet moved any lower. The non-seasonally adjusted Aggregate Composite MLS® HPI was still up by 3.3% on a year-over-year basis in September, a far cry from the near-30% record year-over-year gains logged in early 2022.

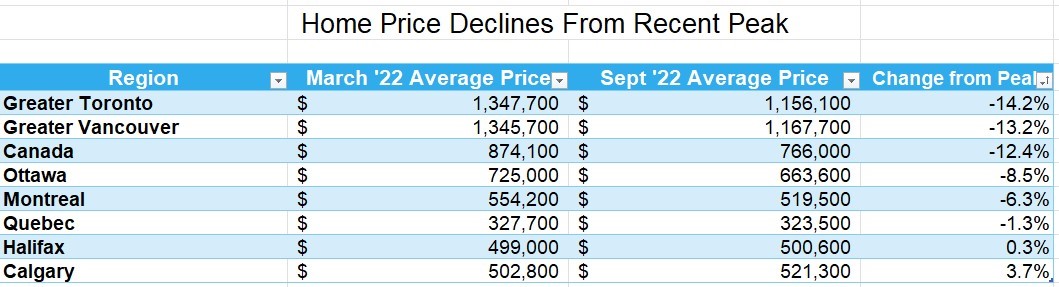

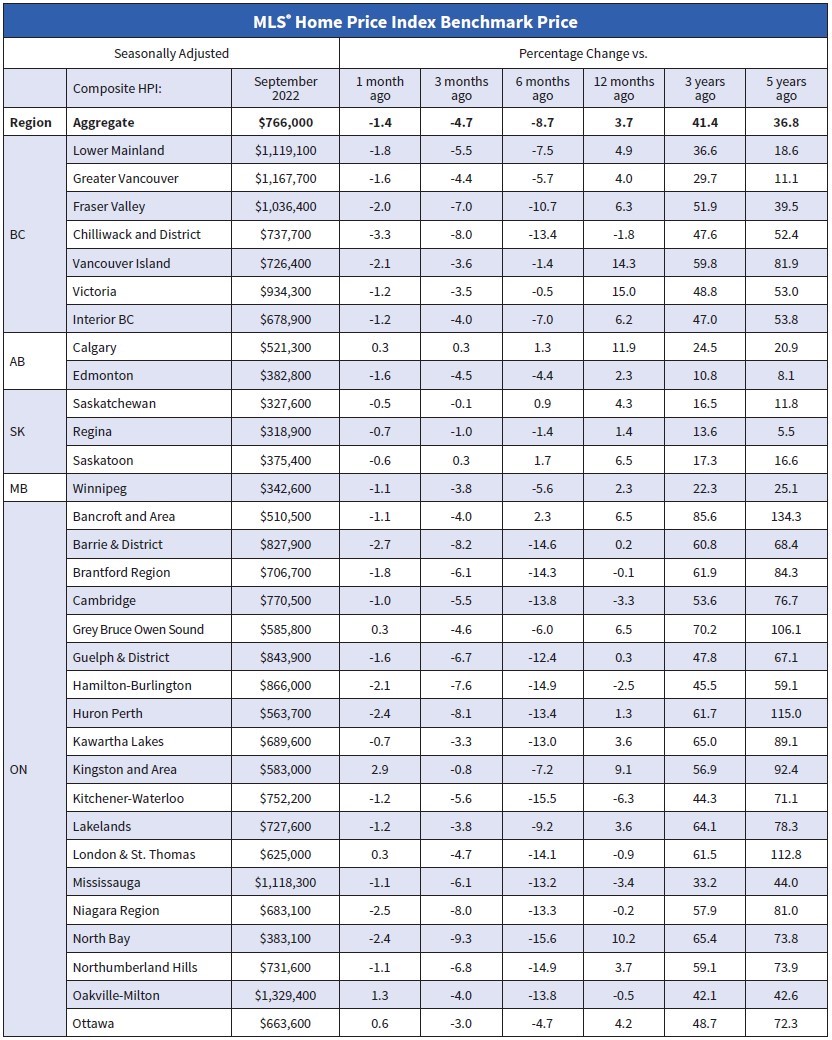

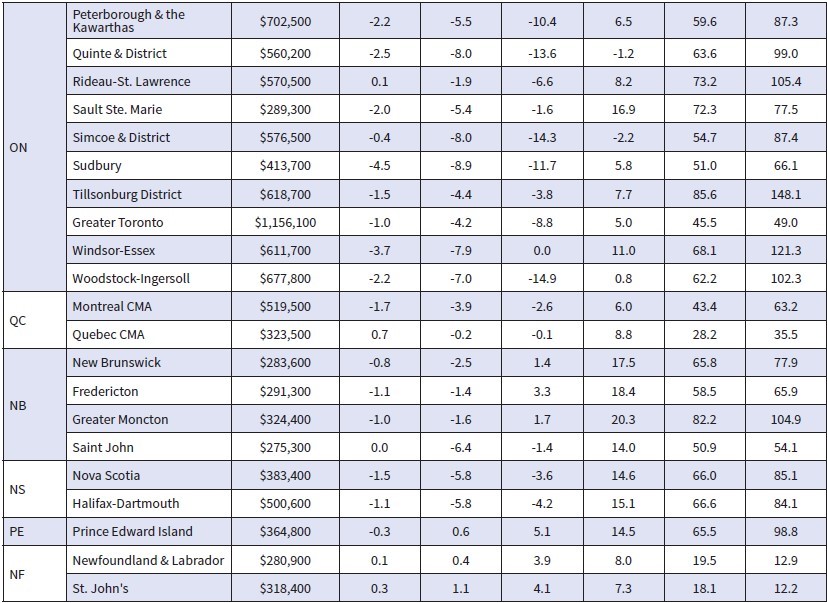

The table below shows the decline in average home prices in Canada and selected cities since prices peaked in March when the Bank of Canada began hiking interest rates. More details follow in the second table below. The largest price dips are in the GTA and the GVA, where the price gains were spectacular during the Covid-shutdown.

US Inflation Surprises on the High Side in September In other news, US CPI data, released yesterday for September, show inflation remains stubbornly high, assuring another 75 bps increase in the US overnight policy rate when the Fed meets again on November 3.

A closely watched measure of US consumer prices rose by more than forecast to a 40-year high last month, pressuring the Federal Reserve to raise interest rates even more aggressively. The core consumer price index, which excludes food and energy, increased 6.6% from a year ago, the highest level since 1982. From a month earlier, the core CPI climbed 0.6%. On the heels of a solid jobs report last week and record-low unemployment, the inflation data likely cement an additional 75-basis point interest rate hike at the Fed’s November policy meeting. Even more noteworthy, however, is that immediately following the release of the inflation report, the market assessment of the maximum overnight rate rose from 4.6% to 4.85% for March of next year, substantially above the current overnight rate of 3.25%.

Bottom Line

The Bank of Canada’s next policy announcement date is October 26, when we will likely see another hike in the overnight policy target of at least 50 bps to 3.75%. Much will depend on next week’s release of the September CPI report for Canada on Wednesday, October 19. All eyes will be on the Bank’s measures of core inflation, which have been stubbornly sticky at above 5% on average. If the data disappoint on the high side, we can’t rule out a 75-bps rate hike the following week.

I believe both the Bank of Canada and the Fed will hike overnight rates further later this year and into next year. They are also not likely to begin to reverse these rate hikes until 2024.

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

When it comes to making your home more eco-friendly, the best place to start is the kitchen!

With all of the hustle and bustle that goes on in this space (as well as the multitude of appliances), this is the ideal area to transform first for maximum effect.

Invest in Long-Lasting Cookware: Switch your Teflon and low-grade cookware out for stainless steel or cast-iron pots and pans for increased longevity.

Consider Your Appliances: With everything from coffee makers to toaster ovens to microwaves and dishwashers, the kitchen is a busy place when it comes to appliances. Swapping these out for energy-efficient models will reduce costs and energy usage, while providing the same results.

Opt for an Energy-Efficient Stove: With a variety of different stoves available on the market, there are plenty of choices when wanting to move to something more energy-efficient! Think gas stoves, induction cooktops, ceramic-glass cooktops or even energy-efficient electric coils.

Consider Practicing Energy-Efficient Cooking: Want to further maximize your efficiency and energy-usage in the kitchen? Stop preheating! With most ovens today, they heat up almost instantly making pre-heating your oven for 20 minutes a waste of time and energy. Some more tips to improve your energy-efficiency when cooking is to consider pressure cooking, BBQing, eating “raw” food such as salads, chilled soups and more.

Use Green Cleaners: Finally, if you’re going to put all the effort into improving your appliances and habits in the kitchen for greener results, you might also want to consider switching your kitchen cleaners to green products. There are dozens of options out there for non-toxic, biodegradable and plant-based cleaners that you can choose from. Your kitchen (and yourself!) will thank you.

This article is courtesy of the October DLC Newsletter

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

Forty-Three Years Ago, I Was Fed Chair Paul Volcker’s Special Assistant

Inflation appears to be book-ending my career. I started my work as an economist in the Research Division of the Federal Reserve Board in Washington, D.C., in the late 1970s. Inflation had been trending higher for years. Neither Arthur Burns nor G. William Miller, the Fed chairmen preceding Volcker, had the fortitude to raise interest rates sufficiently and keep them there long enough to reduce inflation to a low sustainable pace. Paul Volcker pulled it off–for which he was personally vilified at the time. But since then, Paul Volcker has become a legend, esteemed as the central banker whose brute-force campaign subdued inflation for decades.

You can see in the chart below that in late 1979, the Volcker Fed hiked the overnight policy rate to levels well above the inflation rate and kept real interest rates (nominal rate minus inflation rate) positive for an extended period.

The current Fed Chair, Jay Powell, has expressed deep admiration for Paul Volcker, calling him “the greatest economic public servant of the era.” Last month, Powell alluded to his predecessor’s record of persistence, saying that policymakers “will keep at it until the job is done” — invoking Volcker’s memoir, “Keeping at It.”

The Bank of Canada was no slouch on the inflation front as well. As the chart shows, the Bank hiked interest rates in lockstep with the Fed in the Volcker years and even more in the early 1990s when Ottawa was fighting Canadian budgetary red ink to the ground.

This time around, Tiff Macklem has been ahead of the Fed in hiking interest rates and, in a speech on Thursday, said that the economy is still “clearly” in excess demand, with businesses facing an extremely tight labour market, wage gains broadening and underlying inflation pressures showing no signs of letting up. Macklem said that the sources of inflation, which started with goods prices, are broadening to the service sector. “. Labour markets remain very tight. Job vacancies have eased a little in recent months but remain exceptionally high. Our business surveys report widespread labour shortages. And wage growth has risen and continues to broaden.”

“With demand running ahead of supply, competition is posing less of a restraint on price increases, and businesses are passing through higher input costs more quickly. As a result, higher energy and material costs are showing up in the prices of a growing list of goods and services. So even if there is some relief at the gas pumps, price pressures remain high and continue to broaden. In August, the prices of more than three-quarters of the goods and services that make up the CPI were rising faster than 3%.”

Macklem continued, “As we look for a more fundamental turning point in inflation, measures of core inflation are becoming increasingly relevant…after taking out volatile components in the CPI that don’t reflect generalized changes in prices, inflation is running about 5%. That’s too high. We can also see that our core measures have yet to decline meaningfully even though total CPI inflation has come down in the last couple of months. Going forward, we will be watching our measures of core inflation closely for clear evidence of a turning point in underlying inflation.” In conclusion, the governor said, “there is more to be done….We know we are still a long way from the 2% target. We know it will take some time to get there. We also know there could be setbacks along the way, and we can’t afford to let high inflation become entrenched”.

So given the clear statements by the Fed and the Bank of Canada, it makes no sense why Bay Street economists are betting that the overnight rate in Canada will peak at around 4% by yearend. They are still forecasting a decline in short-term interest rates next year due to a slowdown in economic activity. I don’t buy that.

There are many views on how far the central banks will have to hike rates from here, but the critical issue is to reach a point where rates are meaningfully restrictive. A rule of thumb is that the overnight policy rate must rise to exceed the inflation rate. Fed Chairman Powell has said that he believes that real interest rates should be positive across the yield curve. Today, long and short US rates are still the lowest compared to inflation since the Burns era in the mid-1970s. (see chart below). Traders are betting that the US overnight rate will rise another 125 basis points (bps) by yearend and continue to rise next year to a median estimate of 4.6%.

Chair Powell has clarified that he is willing to tolerate much slower growth. As Bloomberg economists suggest, “Canada is seen having both faster growth and lower interest rates over the next three years — a peculiar mix of economic outcomes that assumes the country is more buffered from global headwinds — including a potential US recession — but won’t face the same pressure to match the Fed higher.”

Short-term money markets are betting the Bank of Canada will stop its hiking cycle at about 4%, versus a Fed benchmark rate peaking at about 4.6% and remaining below US short-term rates for at least another three years.

This is especially unreasonable given the fall in the Canadian dollar, which is now trading at US$0.728 compared to US$0.814 one year ago. This depreciation reflects the inordinate strength of the US dollar–the global safe-haven currency in a time of enormous uncertainty and volatility. The Canadian dollar has fared far better than other G-7 countries over this period. But the decline in our currency will raise the prices of the many US products and services we import, adding to inflation.

Inverted Yield Curves

In Canada and the US, 2-year yields have risen sharply to levels well above 5-year yields. As of October 6, the 2-year Government of Canada bond yield is at 4.0% compared to the 5-year yield at 3.49% and the 10-year yield at 3.31%. This implies the markets expect a slowdown in economic activity, but that does not mean that the overnight policy rate will fall in 2023 as Bay Street expects, especially if core inflation remains well above 2%. The Canadian prime rate is currently 5.45%, well above the 5-year yield of 3.49%. When the Bank of Canada Governing Council meets again on October 26, it will likely raise the policy rate by at least 50 bps to 3.75%, taking the prime rate up to 5.95% or higher—clearly improving the relative attractiveness of fixed-rate mortgage loans.

Bottom Line

For most of my readers, inflation is a brand-new experience, and so are rising interest rates. Inflation in Canada was at 2.2% when the pandemic began, and the 5-year bond yield was a mere 1.3%. Quickly the central bank cut the overnight rate from 1.75% to 0.25%, the prime rate fell from 3.95% to 2.45%, and the 5-year bond yield fell to a low of about 0.32%. Housing demand exploded and continued strong until it peaked in February 2022 when the Bank of Canada began to hike interest rates.

Interest rates will not fall to pre-pandemic levels next year or even the year after. And we will likely never see interest rates at pandemic levels again, at least I hope not, because it would take another global economic shutdown. Hence, mortgage-borrower psychology will change. Many more homeowners will choose to lock in fixed interest rates, and by the time this is over, a new generation will realize that interest rates don’t just fall but sometimes rise to levels higher than expected and stay there longer than expected—a painful lesson to learn.

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

With record-high inflation, Canadian shoppers are well aware that the cost of just about everything is going up.

But they can soon expect to see a new demand for their dollars when they shop, because starting Thursday, retailers and other businesses will be allowed to charge them a fee every time they swipe their credit card once notice is provided to card companies.

While consumers love the convenience and rewards of paying with credit cards, they have raised the ire of retailers for years because as part of the original card agreements, stores had to give a percentage of every sale to the card providers for making the transaction happen. The fee can range from fractions of a per cent to more than two per cent for some premium cards.

As part of their card agreement, merchants were forbidden from passing on that cost to consumers. But that all changed earlier this year, when Visa, MasterCard and other card providers settled a long-running lawsuit on the issue in Canada — agreeing torebate merchants $188 million for what are known as interchange fees that merchants were charged in the past decade.

“Credit cards are one of the most expensive means of payment for merchants,” said Luciana Brasil, a partner at Vancouver-based law firm Branch MacMaster LLP, which worked on the class-action lawsuit that led to the settlement.

Customers love paying with cards because “they get their points, their rebates, their benefits,” she said, “but they rarely ask themselves who’s paying for that.

“In reality, the more benefits those credit cards give the consumer, the more expensive they are for the merchant to accept them.”

Many parts of the world, including the European Union, the United Kingdom, Israel, Australia, China and Malaysia, have capped the fees, known as interchange fees, at well under one per cent. Visa says the average interchange fee for its cards in Canada is 1.4 per cent.

Merchants must give 30 days’ notice

Part of the deal Brasil ironed out with credit card companies allows merchants to pass on that cost to consumers directly in the form of a surcharge — which means consumers should get used to seeing it soon.

The new rules won’t be a free-for-all, as starting Thursday, merchants must give card providers 30 days’ notice of their intent to start charging a fee. They must also make it clear to customers at the time of payment that there’s a surcharge, and it can’t be more than they pay themselves. Finally, the surcharge will be capped at 2.4 per cent. But the rules won’t be in force in Quebec, because that type of fee is forbidden under the province’s Consumer Protection Act.

In a poll of nearly 4,000 members of the Canadian Federation of Independent Business (CFIB) conducted in early September, the group found that about one in five small businesses plan to levy the fee, and more than a quarter say they will if their competitors do.

More than one-third say they plan to use other means to try to convince customers to pay using another method, and more than a quarter say they plan to simply increase their prices to cover the cost of credit card payments.

Most small businesses say they don’t want to charge the fee, but with a card provider taking $2 of a $100 sale, they have little option but to levy the surcharge, even if it costs them customers.

“Most smaller merchants are still on the fence or don’t plan to surcharge as they don’t want to risk losing customers,” Corinne Pohlmann, CFIB’s senior vice-president of national affairs and partnerships, said. “But surcharging gives them the ability to offset some of their costs and be transparent with their customers about the fees they pay.”

Entrepreneurs Chris and Nunu Rampen are among those who plan on charging customers a fee for using a credit card, albeit begrudgingly.

“I look favourably on this change because I think it will probably change consumer behaviour,” said Chris, who owns Buna, a downtown Toronto coffee shop, and Nunu, a restaurant, with his wife. “They will think of cheaper methods like either cash — a lot of restaurants just accept cash — or debit, which is much, much cheaper.”

He said interchange fees have long been a thorn in his side, but with the restaurant industry coming out of financial losses sustained during the COVID-19 pandemic, his business is less able than ever to withstand them.

“We’re really in a point of razor-thin margins, and two per cent could matter,” he said. “I don’t see another solution, frankly.”

Consumer choice

Consumers are likely to bristle at the fee, but based on what some of them told CBC News this week, it seems that Rampen’s hope of getting them to choose different payment options is likely to work.

Calgarian Irene Kreitz said a two per cent surcharge is likely enough to get her to take a different card out of her wallet.

“For an additional two per cent … no, I wouldn’t use my credit card, I would use my debit,” she said.

Samantha Cook, also of Calgary, is of a similar mindset. “The cost of living is already fairly high … so with that extra two per cent, I’m more inclined to use my debit card,” she said.

For others, the lure of reward points will likely be enough to keep them using their cards even if a fee is attached. A Bank of Canada report last year found that Canadians racked up $3.4 billion worth of rewards from their credit cards in 2018, with higher-income earners benefiting the most because they are far more likely to use credit cards as payment.

Those rewards come at a steep cost for merchants — more than $11 billion in 2018, the central bank found — but many consumers will be unlikely to give up those perks.

“I rarely pay for travel because of the points,” Calgary resident Lyndsay Powell said. “Every single thing I buy, I don’t even have a debit card that I carry with me [because] I would take … travel points for everything.”

For Chris Rampen, it’s unreasonable for shoppers to get a free ride at the expense of hard-hit small business owners.

“What’s unreasonable is that I’m paying the fees,” he said. “So yeah, I’m very happy that it would be transferred to the people actually making the choice — and they do have a choice.”

This article is courtesy of CBC

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

When it comes to your mortgage application, there are a few things that you should avoid doing while you’re waiting for approval – such as making large purchases (i.e. a new car), applying for new credit, pulling additional credit reports, etc.

Another issue that can come up is the loss of your job…

What you can afford to qualify for in relation to your mortgage depends on your income. As a result, the sudden loss of employment can be quite detrimental to your efforts. So, what do you do?

Should You Continue With Your Mortgage Application?

If you’ve already qualified for a mortgage, but your employment circumstances have changed, your first step is to disclose this to myself, your mortgage professional. As the lender will verify your income prior to closing, your mortgage professional will need to update your file to advise them, otherwise, it may be considered fraud as your application income and closing income would not match.

In some cases, the loss of your job may not affect your mortgage. Some examples include:

You secure a new job right away in the same field as previously. Keep in mind, you will still need to requalify. However, if your new job requires a probationary period then you may not be approved.

If you have a co-signer on the mortgage who earns enough income to qualify for the value on their own. However, be sure your co-signer is aware of your employment situation.

If you have additional sources of income such as income from retirement, investments, rentals or even child support they may be considered, depending on the lender.

Can You Use Unemployment Income to Apply for a Mortgage?

Typically this is not a suitable source of income to qualify for a mortgage with A-lenders, but it may still be an option for alternative or B-lenders. In rare cases, individuals with seasonal or cyclical jobs who rely on unemployment income for a portion of the year may be considered. However, you would be asked to provide a two-year cycle of employment followed by Employment Insurance benefits. Contact me and I can help you look into your options!

What Happens During Furlough?

If you did not lose your job entirely but have instead been furloughed or temporarily laid off, your lender may take a wait-and-see approach to your mortgage application. You would be required to provide a letter from your employer with a return-to-work date on it in this situation. However, if you don’t return to work before the closing date, your lender may be required to cancel the application for now with resubmitting as an option in the future.

Regardless of the reason for the change in your employment situation, one of the most important things you can do is contact me directly to discuss your situation. I would be happy to look at all the options for you and help with finding a solution that best suits you.

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

Whether you’re currently in the process of looking for your first home, or have just started to think about it, I have some first-time homebuyer tips to help make your journey as easy as possible!

Some of these you may already know about, and some you might not, but they are sure to make your first homebuying experience that much easier!

Get Pre-Approved

Having your mortgage pre-approved is an important step in the process and benefits you in three ways:

Pre-approval helps verify your budget and allows your real estate agent to find the best home in your price range. Quick Tip: Don’t forget about the closing costs! These range from 1 to 4% of the purchase price and should be factored into your budget.

Pre-approval guarantees the rate offered and locks it in for up to 120 days. This protects you from any increases in interest rates while you are shopping (phew!). Make sure to ask exactly how long your pre-approval is good for!

Pre-approval lets the seller know that securing financing should not be an issue, which is beneficial in competitive markets!

Keep in mind, this is not the same as final mortgage financing approval, but it can be a very helpful step in the process towards getting your final approval by helping you work within your budget.

Using the My Mortgage Toolbox app can help you get pre-qualified as part of your pre-approval – right from your mobile phone! In addition, this incredible tool can help you calculate your closing costs and even your potential monthly mortgage payments.

Maintain Your Credit

If you are currently looking at homes or thinking about looking at homes, it is vital to maintain your credit throughout the entire mortgage process. Be sure to continue to pay your bills on time, refrain from applying for new credit, closing off credit accounts or committing to any other large purchases (i.e. new car), and also avoid pulling additional credit reports once you have been pre-approved. Another helpful tip is to keep any credit card balances below 70% of the limit to help skyrocket your score!

Utilize Your RRSPs

Did you know? The Home Buyer’s Plan allows you to utilize up to $35,000 from your RRSP and put it towards a down payment on a new home, which you can repay over a 15-year period. You must be a first-time home buyer to qualify.

Take Advantage of Government Programs

There are various government programs in place that provide some financial relief in the form of rebates and tax refunds, including:

First-Time Home Buyer (FTHB) Tax Credit: First-time home owners would get a credit of $1,500 if you qualify. Learn more.

First Time Home Buyer Incentive: The government will cover 5% of the purchase price on a resale home or up to 10% on a newly constructed home, if you qualify. Learn more.

GST/HST New Housing Rebate: You may qualify for a rebate for some of the GST or HST paid on the purchase price or cost of building your new house. Learn more.

There are also additional programs and support available depending on your province that are worth looking into, including land transfer and property transfer rebates, first-time homebuyer tax credits, homeownership support programs and more.

Contact Me for Expert Advice!

Before you get started on your homebuying journey, make sure to reach out to me for expert advice on choosing the right mortgage options, determining your budget, getting your pre-approval, and more!

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

Inflation Cooled Again in August, But Higher Rates Still Coming

Canada’s headline inflation rate cooled again in August, even a bit more than expected. The consumer price index rose 7.0% from a year ago, down from 7.6% in July and a forty-year high of 8.1% in June, mainly on the back of lower gasoline prices.

The CPI fell 0.3% in August, the most significant monthly decline since the early months of the COVID-19 pandemic. On a seasonally adjusted monthly basis, the CPI was up 0.1%, the smallest gain since December 2020. The monthly gas price decline in August compared with July mainly stemmed from higher global production by oil-producing countries. According to data from Natural Resources Canada, refining margins also fell from higher levels in July.Transportation (+10.3%) and shelter (+6.6%) prices drove the deceleration in consumer prices in August. Moderating the slowing in prices were sustained higher prices for groceries, as prices for food purchased from stores (+10.8%) rose at the fastest pace since August 1981 (+11.9%).

Price growth for goods and services both slowed on a year-over-year basis in August. As non-durable goods (+10.8%) decelerated due to lower prices at the pump, services associated with travel and shelter services contributed the most to the slowdown in service prices (+5.5%). Prices for durable goods (+6.0%), such as passenger vehicles and appliances, also cooled in August.

Core inflation–which excludes food and energy prices–also decelerated but remains far too high for the Bank of Canada’s comfort. The central bank analyzes three measures of core inflation (see the chart below). The average of the central bank’s three key measures dropped to 5.23% from a revised 5.43% in July, a record high. The Bank aims to return these measures to their 2% target.

Bottom Line

Price pressures might have peaked, but today’s data release will not derail the central bank’s intention to raise rates further. Markets expect another rate hike in late October when the Governing Council of the Bank of Canada meets again. But further moves are likely to be smaller than the 75 bps-hikes of the past summer.

There is still more than a month of data before the October 25th decision date. The September employment report (released on October 7) and the September CPI (October 19) will be critical to the Bank’s decision. Right now, we expect a 50-bps hike next month.

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.

The Bank of Canada has made it clear they are not done with interest rate hikes. We want to ensure that those up for mortgage renewals in the next 24 months take extra care when navigating the market to ensure the best mortgage strategy.

If a renewal date is coming up for you or a loved one and are looking for ways to navigate this current market, we want to provide the tools you necessary to make the best possible next steps for yourselves.

Join us on Thursday, September, 29th, at 7:00 PM for our Mortgage Renewal Webinar. In it, we will provide all you need to know about mortgage renewals and other mortgage options so you can decide if that is the best path forward in your journey. Whether it is consolidating all your debt, deciding whether to go fixed or variable, or even a reverse mortgage to gain extra financial security in hand.

Follow the link HERE to sign up, completely FREE! Be sure to send in your questions on the sign-up page in advance and we’ll be sure to answer your questions!

The Angela Calla Mortgage Team

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show”and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.caor at 604-802-3983.