Navigating the mortgage market requires more than choosing between a fixed or adjustable rate. Over my 20 years in this industry, I’ve seen how markets and lenders adapt in ways consumers might not expect. Adjustable rates can be a VERY powerful tool, but they come with complexities that borrowers must fully understand before committing.

Our approach at the Angela Calla Mortgage Team is not to say adjustable rates are bad or banks are at fault. Instead, we work to empower borrowers by presenting all qualified options and using our experience to help them make confident, informed decisions they’re comfortable with. For instance, adjustable and variable-rate mortgages often come with significant advantages such as large discounts, low compounding frequencies, and only three months of interest for penalties, as well as the flexibility to easily lock into fixed rates when needed.

Here are some important lessons from recent history that highlight the factors borrowers need to consider:

2015: BoC Rate Cuts That Didn’t Fully Benefit Borrowers

In January and July 2015, the Bank of Canada (BoC) reduced its overnight rate twice, by 0.25% each time (a total of 50 basis points). Despite this, Canadian banks only passed along 0.45% (45 basis points) of the cuts, keeping 0.30% for themselves.

This situation highlighted that central bank decisions don’t always translate directly into borrower savings. That missing 0.30% never made its way back to consumers.

2016: Independent Prime Rate Adjustment by a Major Bank

In 2016, one of Canada’s major banks introduced its own proprietary prime rate, setting it slightly higher than the industry-standard prime rate. While most adjustable-rate borrowers didn’t notice because their payments stayed the same, more of their payments were applied to interest instead of principal.

This independent adjustment demonstrated how lenders can make changes that impact borrowers in ways they may not immediately notice. Adjustable-rate mortgages, where payments change with Prime, and variable-rate mortgages, where the interest rate changes but payments may remain constant, further illustrate how adjustable rates are not all the same in mechanics or benefits.

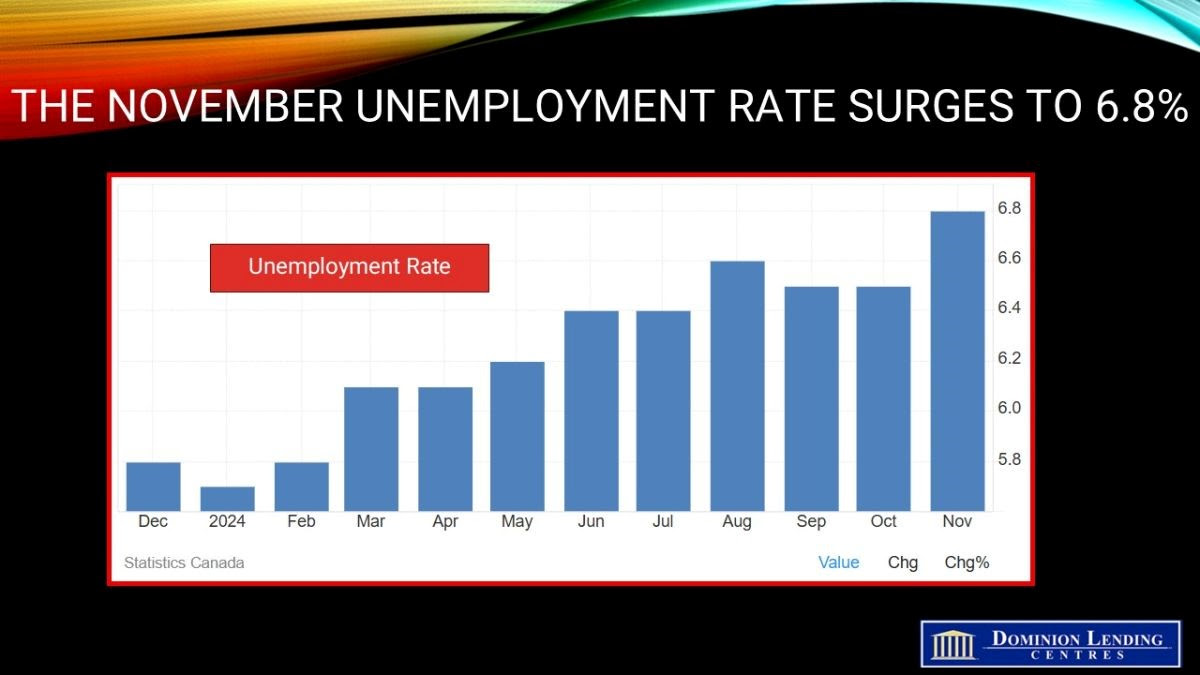

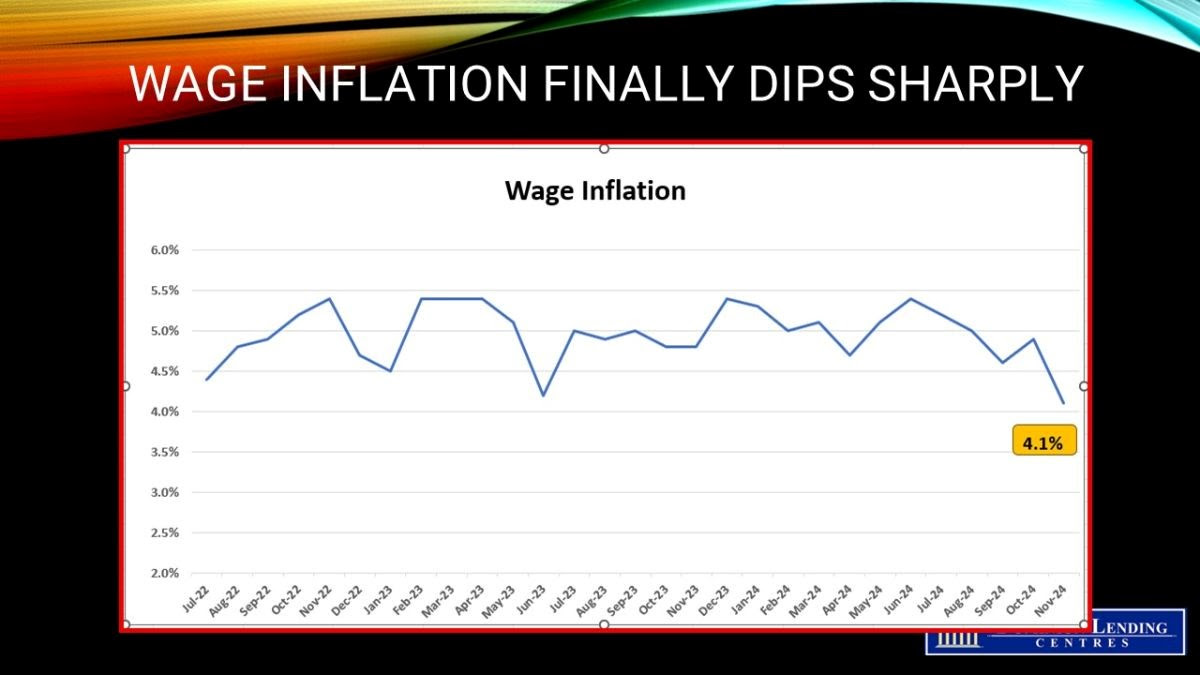

2021-2022: Tiff Macklem’s Reassurance and the Rate Surge

In 2021, Bank of Canada Governor Tiff Macklem assured Canadians that rates would remain low for a prolonged period. This led many borrowers to choose variable-rate mortgages, believing they’d benefit from sustained savings.

However, by 2022, the BoC raised rates rapidly to combat inflation, pushing them to the highest levels in over a decade. Borrowers with adjustable-rate mortgages (ARMs) faced significant payment increases, while variable-rate mortgages hit trigger rates, leading to grossly extended amortization periods in some cases.

Rapid Rate Movements and Market Surcharges

When rates move quickly, lenders may also surcharge adjustable-rate offerings. For example, instead of offering Prime – 0.50%, lenders might adjust to Prime – 0.10% or even Prime + 0. This means the actual discount off prime becomes less favourable, directly impacting borrowers’ costs.

Evaluating the actual discount from prime, rather than focusing solely on the rate, is critical when considering adjustable-rate mortgages.

Financial Empathy During Uncertain Times

In industries prone to strikes or sudden income changes, lenders vary widely in their approach to financial empathy. Some lenders are quick to damage a borrower’s credit score or refuse to renew existing mortgages during difficult times. Others show understanding by offering deferred payment options to help borrowers weather financial challenges.

With our ever-changing market, assessing a lender’s flexibility and empathy is a vital part of the evaluation process. These factors, along with rate comparisons, go into the discussions we have with clients to ensure they’re set up for success in any scenario.

What You’ll Learn in The Mortgage Code

I explore these topics and more in my book, The Mortgage Code. This guide gives borrowers the tools they need to navigate the mortgage market with confidence, helping them understand how factors like market shifts, lender policies, and economic uncertainty can affect their financial future.

Order The Mortgage Code on Amazon. https://www.amazon.ca/Mortgage-Code-Helping-Property-Mistakes-ebook/dp/B07HFHR8TV

Key Takeaways for Borrowers

Understand the risks and rewards: Adjustable rates can offer flexibility and savings, but they come with unpredictability.

Evaluate lender policies: Consider how your lender handles deferred payments, renewals, and financial hardships.

Stay informed about rate discounts: The actual discount off prime, lock-in policies, and penalties matter in addition to just the rate itself.

Work with a trusted advisor: Our experience ensures every aspect of your financial situation is considered, not just the numbers.

Mortgage decisions are more than just choosing between fixed and adjustable rates—they’re about finding the right fit for your life and goals. Let’s work together to ensure you have clarity and confidence in every decision.

Angela Calla is an 19-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.