Bank of Canada Holds Steady…for now!

I hope you have had a fabulous summer. While September will have no decrease in the Bank of Canada prime rate, there is room for variable rates to move down. Here is the full report from today Bank of Canada release and the next meeting is Oct 30th 2019.

It is being speculated that we could see up to a 50 basis point decrease in the next 6 months.

What does this mean for consumers?

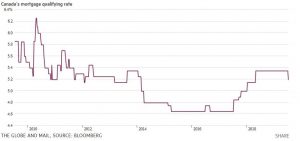

Since 2016, lenders started breaking the norm in terms of discounts being passed along to consumers as they were keeping larger cuts for themselves to help with the reduced revenue due to the new mortgage rule changes and speculation taxes coming into place. I have written in detail about this in my book The Mortgage Code which helps provide clarity on how lenders operate and how to use it to your benefit. Click here to purchase

I suspect that while the Bank of Canada generally does .25 per cent increases or decreases, we will only see a .15 or point.10 discount once the banks decide what to do with their prime as a result should there be a decrease in upcoming months.

An important metric to keep in mind is that every 5 basis points in mortgage amount per $100,000 is $3 a month in difference

For example, a .25 basis point decrease on a $350,000 mortgage would be $50 a month in reduction. A .15% decrease works out to $30 a month decrease.

While the BOC prime is key in determining bank prime, one thing to keep in mind is fixed rates are at record lows.

With the banks using the bond markets to determine fixed rates and people looking for more financial stability, the demand for bonds goes up. While the prime might be going down, it’s possible we might see an increase in the fixed rate.

To optimize the market to your advantage consider this:

1. If you’re thinking of a home purchase, get a pre-approval in place, not just a pre-qualification.

2. If you have a mortgage rate over 3.5%, let’s review to see what the numbers would be with your specific scenario to see if a modification would benefit you to secure a lower rate for a longer period of time. If you are in a variable- let’s review your options for discount vs fixed.

3. If you have debt outside of your mortgage, let’s review if it’s advantageous to add that into your existing mortgage.

4. If you have a mortgage renewal coming up, get the rate held and watch the market until three weeks before completion to see what options become available.

My team is here to help you navigate this ever changing market.

Angela Calla is a 15 year award-winning woman of influence mortgage expert. Alongside her team, passionately assisting mortgage holders get the best mortgage, and educating them on The Mortgage Show on CKNW for over a decade and through her best-selling book The Mortgage Code available on Amazon. To purchase the book click here: The Mortgage Code. Proceeds from all sales will help build a new emergency room at Eagle Ridge Hospital. Angela can be reached at callateam@dominionlending.ca or 604-802-3983.