In light of the recent nose dive mortgage rates have taken, it’s a great opportunity to potentially save money, especially in these 4 stages of life.

- Looking to make a property purchase or renovation

- Have a mortgage renewal upcoming

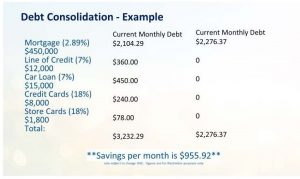

- Have debt outside of your mortgage with interest over 3%

- Anyone who has a mortgage over 3.09% its time to review

If you or someone you care about want to see if these recent changes can help you please call us at 604-802-3983 or email us at: callateam@dominionlending.ca

Here is the clip: COVID-19 Concerns Spark Bank of Canada Rate Cut

Exciting news, last week I had the honour as being announced as a official nominee for the YWCA Woman of Distinction Award.

More details here: YWCA WODA

Other links you may find helpful:

Our Facebook page: https://www.facebook.com/angelacallamortgageteam/

Our Mobile App: https://www.dlcapp.ca/app/angela-calla

Angela Calla is a 16 year award-winning woman of influence mortgage expert. Alongside her team, passionately assisting mortgage holders get the best mortgage, and educating them on The Mortgage Show on CKNW for over a decade and through her best-selling book The Mortgage Code available on Amazon. To purchase the book click here: The Mortgage Code. Proceeds from all sales will be donated to Access Youth Outreach Services. Angela can be reached at callateam@dominionlending.ca or 604-802-3983.