Welcome to the August issue of my monthly newsletter!

I hope you’ve had a fantastic summer so far! This month, I am excited to give you some tips on paying off your mortgage faster. Plus, learn my favourite ways to cut energy costs and save. Scroll down for all the details and have a great month!

How to Pay Off Your Mortgage Faster

When it comes to homeownership, many of us dream of the day we will be mortgage-free. While most mortgages operate on a 25-year amortization schedule, there are some ways you can pay off your mortgage quicker!

Did you know? There are a few ways you can help pay off your mortgage faster

For example – switching to an accelerated bi-weekly payment schedule, increasing your monthly mortgage payments to pay more to the principal, making extra payments on your mortgage, negotiating a better rate, or refinancing to a shorter amortization period!

Let’s take a look at the options and how they work:

- Review Your Payment Schedule: Taking a look at your payment schedule can be an easy way to start paying down your mortgage faster, such as moving to an accelerated bi-weekly payment schedule. While this will lead to slightly higher monthly payments, the overall result is approximately one extra payment on your mortgage per calendar year. This can reduce the total amortization by multiple years, which is an effective way to whittle down your amortization faster.

- Increase Your Mortgage Payments*: This is another fairly simple change you can execute today to start having more of an impact on your mortgage. Most lenders offer some sort of pre-payment privilege that allows you to increase your payment amount without penalty. This payment increase allowance can range from 10% to 20% payment increase from the original payment amount. If you earned a raise at work, or have come into some money, consider putting those funds right into your mortgage to help reduce your mortgage balance without you feeling like you are having to change your spending habits.

- Make Extra Payments*: For those of you who have pre-payment privileges on your mortgage, this is a great option for paying it down faster. The extra payment option allows you to do an annual lump-sum payment of 15-20% of the original loan amount to help clear out some of your loans! Some mortgages will allow you to increase your payment by this pre-payment privilege percentage amount as well. This is another great way to utilize any extra money you may have earned, such as from a bonus at work or an inheritance.

- Negotiate a Better Rate: Depending on whether you have a variable or a fixed mortgage, you may want to consider looking into getting a better rate to reduce your overall mortgage payments and money to interest. This is ideally done when your mortgage term is up for renewal and with rates starting to come back down, it could be a great opportunity to adjust your mortgage and save! This may be done with your existing lender OR moving to a new lender who is offering a lower rate (known as a switch and transfer).

- Refinance to a Shorter Amortization Period: Lastly, consider the term of your mortgage. If you’re mortgage is coming up for renewal, this is a great time to look at refinancing to a shorter amortization period. While this will lead to higher monthly payments, you will be paying less interest over the life of the loan. If you’re interested in this, connect with me today so we can calculate if it is worthwhile for you to take advantage! Knowing what you can afford and how quickly you want to be mortgage-free can help you determine the best new amortization schedule.

*These options are only available for some mortgage products. Check your mortgage package or reach out to me to ensure these options are available to you and avoid any potential penalties.

If you’re looking to pay your mortgage off quicker, don’t hesitate to call me to go over your options in more detail today!

Smart Ways to Cut Your Energy Costs

In the last decade, climate change and energy efficiency have become top of mind for many Canadians. From wanting to do our part by recycling to making our home as energy efficient as possible, there are so many benefits to being environmentally and energy conscious.

If you are looking to cut costs or simply want to reduce your eco-footprint, here are some great ways to cut your energy costs:

- Get a Smart Thermostat: A pretty easy installation, a smart thermostat can help you better manage your in-home temperature. Whether you opt to install a basic programmable thermostat or try Google’s Nest, which learns from you and works to predict which temperatures you prefer and when, getting a read on your in-home temperature can help you better manage your energy usage.

- Look for Drafty Spots: When it comes to heating your home, it can quickly become a wasted effort and results in extra costs if you have drafts in your home. In addition to windows and doors, you should also seal any folding attic stairs, add a fireplace plug to seal the damper and install a dryer vent seal to reduce drafts in your laundry room.

- Swap to LEDs: Most of us are already using LED bulbs throughout our home. If you aren’t yet, now is the time to make the switch! LED bulbs use 15% less energy than an equivalent incandescent, which can save you a ton of money each month especially in larger homes.

- Turn Down Your Water Heater: While sometimes nothing beats a good scalding shower, you don’t want to be burned with a high energy bill. Did you know if you knock down that temperature gauge by just 10 degrees, you can save 3% to 5% on your bills each month!?

- Examine Your Appliances: Since 1992, ENERGY STAR® has been backing energy efficient appliances and products, helping consumers make the right choices. Some of the least green appliances in your home are your dishwasher, washing machine, dryer and refrigerator and, if you don’t currently have Energy Star certified versions of these machines, swapping to them is a surefire way to reduce your monthly expenses.Can’t afford new appliances? Here are some other tips and tricks to help make them more efficient in the meantime:

- Dishwasher: Use a citric acid-based cleaner in an empty cycle to rid your dishwasher of excess soap and calcium buildup that may be causing your machine to work harder.

- Washing Machine: Maximize energy by stuffing your machine to the brim whenever possible as washing machines typically use the same amount of energy regardless of load size.

- Dryer: For starters, ensure you are always cleaning out your lint filter to increase air circulation. In addition, keep an eye on the outside exhaust and clean when needed to reduce drying time and save energy.

- Refrigerator: While most of us are more concerned with the food inside our fridges than the parts, it is important to check your condenser coils. Over time, dirt, food particles and dust can collect and reduce the efficiency. Another tip is to set your refrigerator to 2-3 degrees Celsius.

- Close The Blinds: When the temperature starts heating up, it is important to close the blinds and drapes to prevent the sun from beating in and warming up your home. The excessive heat makes your air conditioner work overtime causing your energy bills to skyrocket.

In addition to the cost savings and environmental benefits of improving your energy efficiency, CMHC also has a rebate available! The CMHC Eco Plus refund can provide a 25% partial premium refund if you’re CMHC insured and buying or building an energy-efficient home! Click here for more details.

Economic Insights from Dr. Sherry Cooper

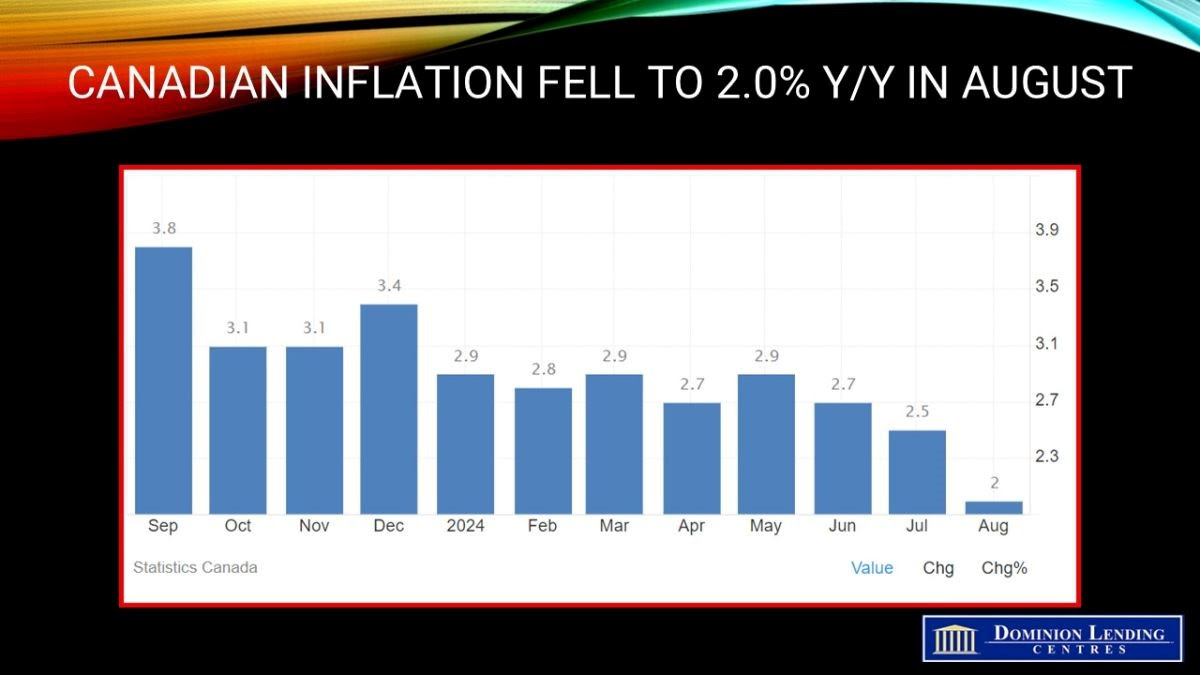

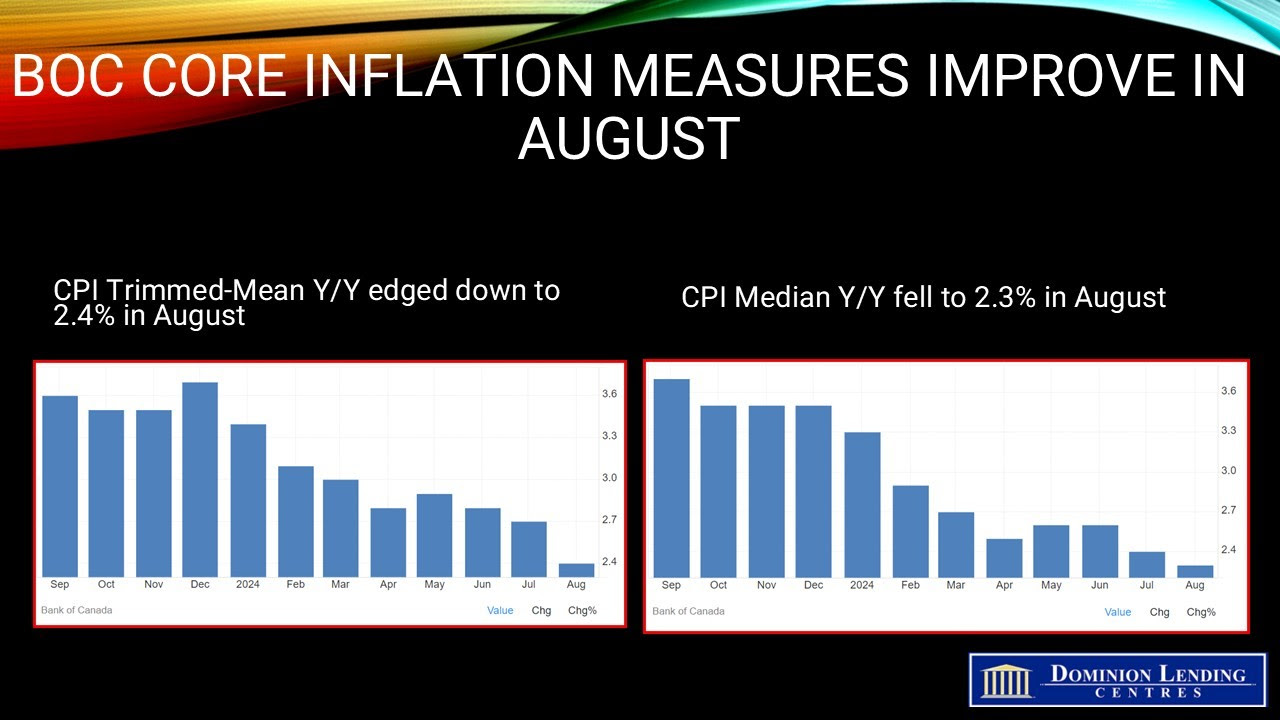

All eyes were on The Bank of Canada last month as they cut interest rates by 25 basis points again during their July 24th meeting, thereby taking the overnight policy rate down to 4.5%.

We believe that owing to a sustained deceleration in inflation, the central bank will continue its monetary easing at the September and December meetings and well into next year.

The policy rate will likely fall to 2.75% next year, reducing the burden of higher monthly mortgage rates on renewals in the next 18 months.

The influx of roughly 2 million immigrants to Canada has raised overall consumer spending, averting a recession this year, but GDP per capita continues to decline.

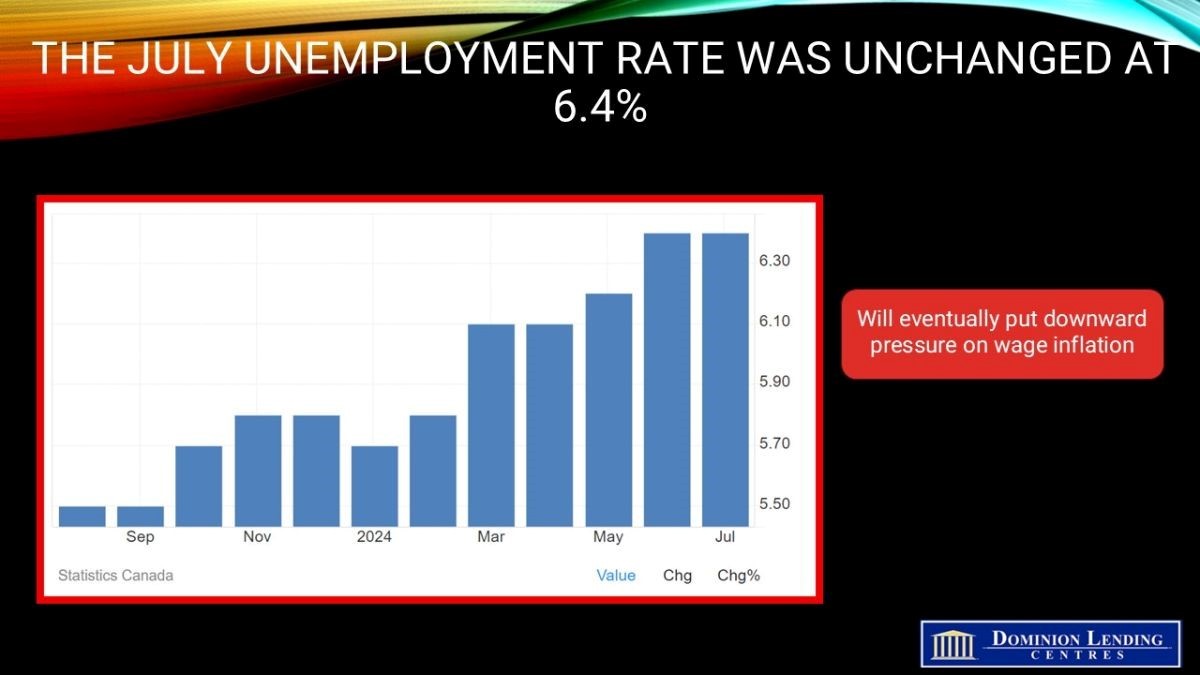

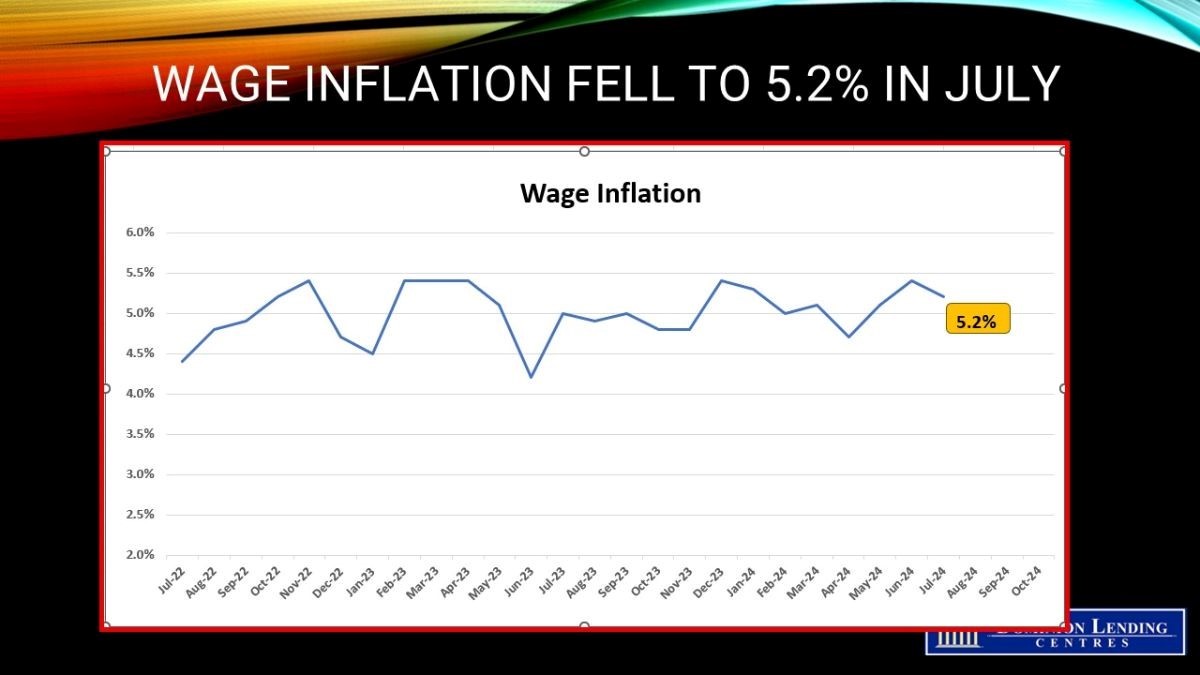

Labour markets continue to soften as job vacancies have fallen sharply, and the jobless rate has risen from 4.9% to 6.4%. The latest business and consumer surveys have suggested that inflation expectations have fallen and wage inflation—a lagging indicator—will soon decline. Companies expect to cut their spending on machinery and equipment, and commercial real estate valuations have fallen owing to the sharp rise in office vacancy rates.

Housing market activity has slowed with the run-up in interest rates from March 2022 until June 2024. Lower interest rates will spur transactions and increase new listings next year. Housing affordability will improve as price pressures remain muted. The housing shortage, however, will likely mitigate the improvement, particularly as the shortage of experienced construction workers impedes rapid housing supply increases.

Angela Calla is an 19-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.