US Policymakers Take Emergency Action To Protect Depositors At Failed Banks

Silicon Valley Bank (SVP) had a sterling reputation among the many tech start-ups it helped to finance. What brought SVB down was an old-fashioned bank run set off in 2021 by a series of bad decisions.

That year, the stock market boomed, interest rates were near zero, and the tech sector was flush with cash. Many start-ups held their working capital and other cash at SVB. The Santa Clara, Calif.-based lender saw total deposits mushroom to nearly $200 billion by March 2022, up from more than $60 billion two years earlier.

The bank invested much of that cash in long-dated Treasury bonds–normally considered a blue-chip investment. If held to maturity, the full value of the initial investment would have been returned to the bank. However, interest rates have risen dramatically since last March, causing the price of those bonds marked-to-market to decline precipitously. SVB risked large losses if it had to liquidate its securities portfolio.

This created a massive mismatch between the value of the deposits and its bond holdings. Moreover, this was not initially transparent to the depositors thanks to a 2018 relaxation of banking regulation much-favoured by SVB’s CEO. Regional banks were no longer required to mark their assets to market, nor were they required to succumb to the regular stress testing by the federal regulator where they prove they could survive black swan events. In addition, capital requirements became easier for these institutions.

In 2018, Trump eased oversight of small and regional lenders when he signed a sweeping measure designed to lower their costs of complying with regulations. An action in May 2018 lifted the threshold for being considered systemically important — a label imposing requirements including annual stress testing — to $250 billion in assets, up from $50 billion.

SVB had just crested $50 billion at the time. By early 2022, it swelled to $220 billion, ultimately ranking as the 16th-largest US bank.

In 2015, SVB Chief Executive Officer Greg Becker urged the government to increase the threshold, arguing it would otherwise lead to higher customer costs and “stifle our ability to provide credit to our clients.” He said that with a core business of traditional banking — taking deposits and lending to growing companies — SVB doesn’t pose systemic risks.

Another unique problem for SVB was the unusual concentration of deposits from certain types of clients. SVB’s depositors were heavily concentrated in the tight-knit world of start-ups and venture capitalists (VCs). In the past few weeks, VCs, founders, and other wealthy customers on social media and in private chats started discussing concerns that SVB could no longer pay its depositors. Some began to move their money out of the bank, triggering a loss of confidence and a run on the bank.

A Rapid Fall

On Friday, Silicon Valley Bank became the biggest US bank to fail since the 2008 financial crisis.

Another beneficiary of easing regulatory oversight of small and midsize regional banks was New York-based Signature Bank, which also suffered a massive withdrawal of deposits. On Sunday, regulators shut down Signature, fearing that sudden mass withdrawals of deposits had left it on dangerous footing.

The back-to-back bank failures unnerved investors, customers and regulators, harkening back to the financial crisis in 2008, which toppled hundreds of banks, led to enormous taxpayer-financed bailouts, and sent the US and many other countries into a severe recession.

Canada, on the other hand, escaped much of the pain, experiencing a mild short recession. Although Canadian bank stocks plunged, our banking system was lauded worldwide as a regulatory example for the rest of the world.

Regulators Rush to Forestall Widespread Bank Runs

US Federal regulators scrambled to defuse the situation over the weekend, announcing on Sunday that all depositors would be paid back in full.

The Federal Reserve, Treasury and Federal Deposit Insurance Corporation announced in a joint statement that “depositors will have access to all of their money starting Monday, March 13.” To assuage concerns about who would bear the costs, the agencies said that “no losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.”

The agencies also said they would make whole depositors at Signature Bank, which the government disclosed was shut down on Sunday by New York bank regulators. The state officials said the move came “in light of market events, monitoring market trends, and collaborating closely with other state and federal regulators” to protect consumers and the financial system.

The President said on Sunday and Monday, “I am pleased that they reached a prompt solution that protects American workers and small businesses and keeps our financial system safe. The solution also ensures that taxpayer dollars are not put at risk.”

He added: “I am firmly committed to holding those responsible for this mess fully accountable and to continuing our efforts to strengthen oversight and regulation of larger banks so that we are not in this position again.”

The collapse of Signature marks the third significant bank failure within a week. Silvergate, a California-based bank that made loans to cryptocurrency companies, announced last Wednesday that it would cease operations and liquidate its assets.

Amid the wreckage, the Fed also announced that it would set up an emergency lending program, with approval from the Treasury, to funnel funding to eligible banks and help ensure that they can “meet the needs of all their depositors.”

The additional funding will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

The F.D.I.C. is usually supposed to clean up a failed bank in the cheapest way possible, but regulators agreed that the situation posed a risk to the financial system, which allowed them to invoke an exception to that rule. The regulator will tap the Deposit Insurance Fund, which comes from fees paid by the banking industry, to ensure it can pay back depositors.

The agencies said that “any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.”

Monday’s Market Meltdown

Not surprisingly, the stock markets around the world opened sharply lower on Monday. The previous day, Goldman Sachs said that any Fed rate hikes were off the table for March 22 (I disagree). Bank stocks and energy stocks were hardest hit in virtually all markets. On the other hand, bonds surged, taking interest rates down sharply.

When banks collapse, others sometimes fear their banks and investments will follow. Even healthy banks don’t keep enough cash to pay out all depositors. So, if too many people panic at once and pull out their money — a classic bank run — it could lead to broader financial and economic calamity. And that is what the Biden administration and the Federal Reserve are trying to stop: a financial crisis prompted mainly by plunging confidence.

Canada’s Banks Are In Much Better Shape

Although most Canadian bank stocks plunged on Monday, the regulatory environment is far tighter than in the US. Moreover, Canadian banks are dominated by the Big Six rather than the thousands of banks in the US. They have nationwide branch networks with a large diversified base of clients with less exposure to technology, fewer deposit runoff issues and higher ratios of loans to deposits.

There is much less hot money coming into the Canadian banks than the small and midsize regional lenders in the US that focus on a specific niche part of the loan and deposit markets. Canadian banks are also much better capitalized.

Finance Minister Chrystia Freeland met with Canada’s superintendent of federal financial institutions, Peter Routledge, one day after his office announced it had seized control of SVB Financial Group’s branch in Canada.

SVB’s Canadian arm is unusual because it has a license to lend but cannot take deposits. While some Canadian startups had deposited with the bank’s U.S. arm, the Canadian operation held no client money.

SVB is a small lender in Canada. The tech financer had US$692 million in assets and US$349 million in outstanding loans in Canada as of December, according to OSFI filings. CIBC had $2.9 billion in loans through its innovation banking arm as of October 31, 2021. A bank looking to bolster its lending to startups could scoop up SVB’s loan book at a steep discount.

Yields in Canada fell sharply, following the Treasury market’s lead. Investors reversed course and bet the Bank of Canada will start cutting rates soon.

OSFI has already taken action to monitor daily the liquidity of Canadian banks in the wake of the SVB failure.

Bottom Line

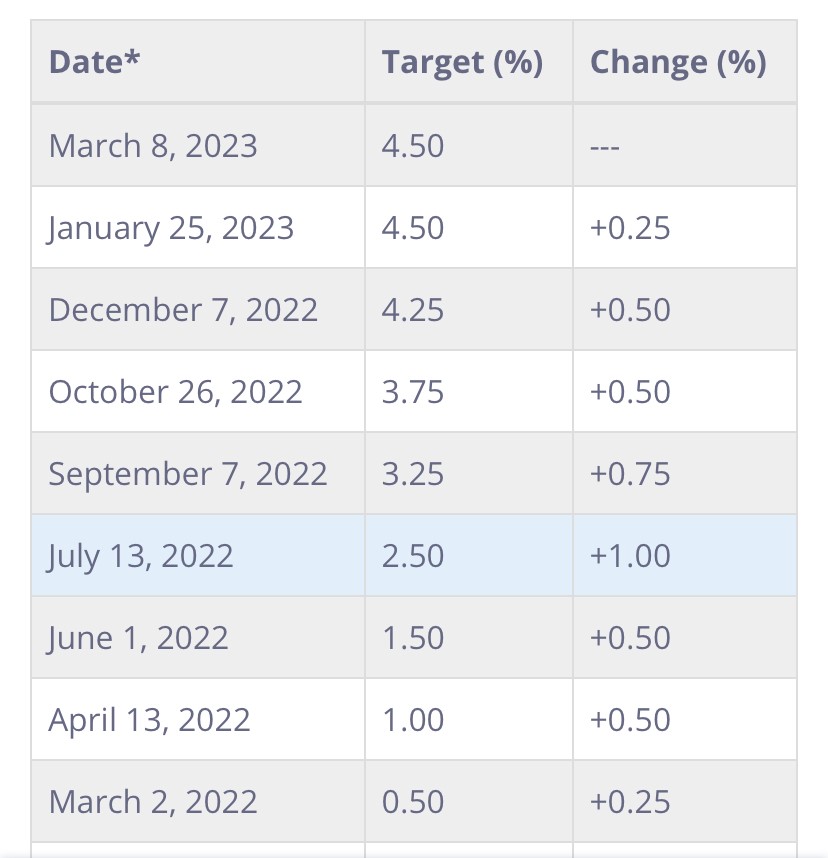

Goldman Sachs was virtually alone when it said it expects the central bank to pass up the chance to hike interest rates next week. Markets still expect the Fed to keep up its inflation-fighting efforts, despite high-profile bank failures that have rattled the financial system. Traders on Monday assigned an 85% probability of a 0.25 percentage point interest rate increase when the Federal Open Market Committee meets March 21-22.

Surging bond yields played into the demise of SVB in particular as the bank faced some $16 billion in unrealized losses from held-to-maturity Treasurys that had lost principal value due to higher rates.

Is this enough to qualify as the kind of break that would have the Fed pivot? The market overall doesn’t think so.

For a brief period last week, markets were expecting a 0.50-point move following remarks from Fed Chair Jay Powell indicating the central bank was concerned about recent hot inflation data (see chart below).

Bank of America and Citigroup said they expect the Fed to make the quarter-point move, likely followed by a few more. Moreover, even though Goldman said it figures the Fed will skip a hike in March, it still is looking for quarter-point increases in May, June and July.

Next week’s meeting is a big one in that the FOMC will not only decide on rates but also update its projections for the future, including its outlook for GDP, unemployment and inflation.

The Fed will get its final look at inflation metrics this week when the Labor Department releases its February consumer price index on Tuesday and the producer price counterpart on Wednesday. A New York Fed survey released Monday showed that one-year inflation expectations plummeted during the month.

Angela Calla is an 19-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.