The Canadian mortgage market is at the precipice of an evolutionary shift as it ventures into a post-pandemic environment.

With the 2023 Residential Mortgage Industry Report from the Canada Mortgage and Housing Corporation (CMHC) now available, CMHC 2023 Residential Report

a roadmap has been provided for the mortgage industry moving forward, outlining crucial insights into future prospects for real estate professionals of all stripes.

An important trend emerging from the report is the prominent ascent of non-bank lenders, a significant factor contributing to a transformative shift in the mortgage landscape. These lenders have been increasing their hold on the market share thanks to their competitive rates and flexible terms, which cater to a broad spectrum of borrowers. As these non-bank entities continuously innovate and remodel themselves to cater to dynamic consumer needs, we foresee them becoming progressively influential players in the mortgage arena.

Another central agent of change in the mortgage industry is the emergence of new technology, including AI. The CMHC report underscores the growing role of digital platforms in the mortgage approval process. This trend, catalyzed and expedited by the pandemic, has streamlined the mortgage process, making it quicker, more efficient, and, importantly, more accessible for borrowers. In the future, we envisage technology taking further leaps, with artificial intelligence and machine learning assuming a crucial role in risk evaluation and decision-making.

Government policies will invariably persist in molding the future shape of the mortgage market. The government’s pandemic response significantly impacted mortgage lending practices, especially its provisions to buttress homeowners and stimulate the housing market. As we navigate the road ahead, we expect government policies to keep pace with fluctuating market conditions, emphasizing stability and mitigating potential risks.

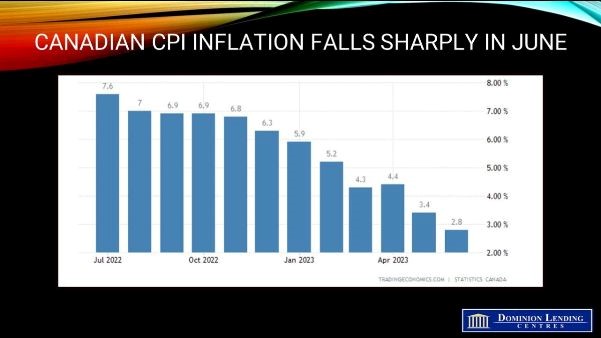

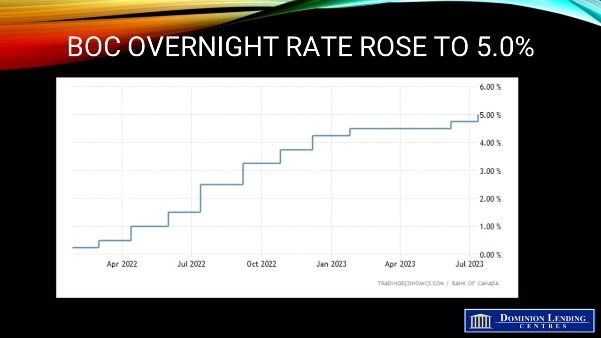

Though the Bank of Canada chose to pause rate hikes earlier in 2023, there has been growing speculation that increases in lending rates could be on the way. As the conditions the BoC laid out for pausing the rate hikes are no longer being met due to stronger-than-expected GDP numbers and an increasing inflation rate, we could expect another rate hike by the end of the year. That said, the overall outlook for the remainder of the year will likely be contingent on regional conditions, with smaller, presently affordable markets likely to maintain their stability.

Nevertheless, these shifts are not devoid of challenges. The growing presence of non-bank lenders and the mounting reliance on technology in the mortgage process could inadvertently lead to an increased risk quotient in the housing market. Regulatory bodies must keep a close watch on these developments and stand ready to intervene as needed to uphold market stability.

In conclusion, the future of the Canadian mortgage market will likely be sculpted by intensifying competition, rapid technological advancements, and flexible government policies. As we traverse this ever-changing landscape, it will be vitally important for borrowers to stay informed and collaborate with trusted professionals to make prudent decisions for their financial future. With an increasingly complex and dynamic mortgage industry landscape, we are on the cusp of an era that could define the future of housing finance in Canada for years to come.

Angela Calla is an 19-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.