|

|

|

Interest Rates & Payment Increases: The Actual Math

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General Angela Calla 6 Oct

|

|

|

Interest Rates & Payment Increases: The Actual Math

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General Angela Calla 24 Aug

Take a look at Angela Calla’s awesome article in the September 2015 issue of the CMP magazine. CLICK HERE to view the article

Want to ensure you have the best mortgage? The Angela Calla Mortgage Team can help you directly at 604-802-3983 or callateam@dominionlending.ca. Contact us today!

General Angela Calla 22 Aug

Hear Stu’s story, a Doctor from Langley who got helped by #callateam to redo his #mortgage. Stu is a repeat client and we are glad we were able to save him thousands. Click HERE to listen to the full testimonial

General Angela Calla 29 Jul

You guys are my people, I am so impressed with you guys so far. I almost fell off my seat when I opened Angela’a hand written letter to me, thanking me and her little present. it is so refreshing to see her personal attention is this form letter world we live in. thank you so much Angela. you are your team are great people.

talk soon,

James

General Angela Calla 28 Jul

Great news from the Financial Post announcing that Canada Mortgage and Housing Corp. is going to make it easier for homeowners renting out apartments in their principal residences to borrow money, a move that could further heat up markets in Toronto and Vancouver. Read the full article HERE

The Angela Calla Mortgage Team gives you clarity on the best mortgage by being transparent, unbiased free mortgage advise with choice. We are here to help you personally with your mortgage at 604-802-3983 or callateam@dominionlending.ca

General Angela Calla 28 Jul

Ryan and Laura sent us a pretty moving testimonial. turn up your speakers!

Click HERE to view the youtube video

Want to ensure you have the best mortgage? The Angela Calla Mortgage Team can help you directly at 604-802-3983 or callateam@dominionlending.ca. Contact us today!

General Angela Calla 28 Jul

The level of support and care we received from Angela, Graeme, John and the rest of the Calla Team was by far the best we have ever experienced! They were very easy to communicate with and very prompt with their replies whether it was through email or phone. They took the time to thoroughly educate, explain and clarify our mortgage and other financial details to put us in the best situation to save the most money as possible. We are really appreciative and truly grateful for the level of service we received (and will receive in the future).

Jonathan from Surrey

General Angela Calla 26 Jul

|

Are you a happy Angela Calla Mortgage Team client? We have just launched an exciting new contest – #ThanksDLC – and I want to invite you to enter to win a cash prize! All you have to do is submit a short video (30 to 60 seconds) about your experience working with my team. Did we exceed your expectations when I helped you get the best possible mortgage? Did you like that there was no fee for my service? How about how easy it was to work with the Angela Calla Mortgage Team? Ten videos will be selected and then be made into professionally shot TV commercials. PLUS all ten finalists will earn a cash prize! Here’s how you get started: |

|

|

Next, think about all the great things you can buy for your beautiful home with the $5,000 top prize or one of the nine $1,000 semi-finalist awards. Of course, you will have to put up with all the fame and glory that comes along with Dominion Lending Centres turning your video into a nationally broadcast TV commercial! |

|

|

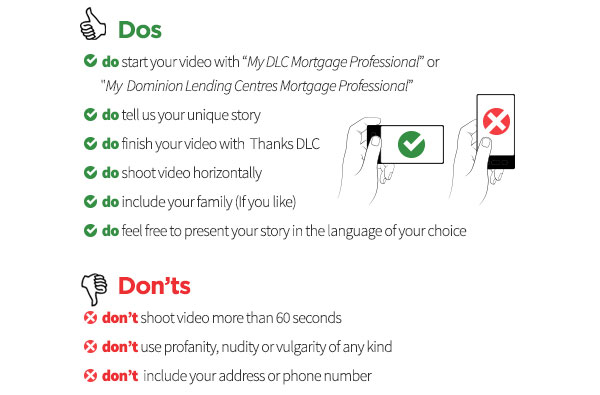

Finally, here are some simple DO’s and DON’T’s so you have the best chance of winning one of the prizes: |

|

|

This is an exciting contest and I cannot thank you enough for getting involved! Good luck and If you have any questions, please let me know. |

|

General Angela Calla 23 Jul

|

||

|

Are you a happy Angela Calla Mortgage Team client? We have just launched an exciting new contest – #ThanksDLC – and I want to invite you to enter to win a cash prize! All you have to do is submit a short video (30 to 60 seconds) about your experience working with my team. Did we exceed your expectations when I helped you get the best possible mortgage? Did you like that there was no fee for my service? How about how easy it was to work with the Angela Calla Mortgage Team? Ten videos will be selected and then be made into professionally shot TV commercials. PLUS all ten finalists will earn a cash prize! Here’s how you get started: |

||

|

||

|

Next, think about all the great things you can buy for your beautiful home with the $5,000 top prize or one of the nine $1,000 semi-finalist awards. Of course, you will have to put up with all the fame and glory that comes along with Dominion Lending Centres turning your video into a nationally broadcast TV commercial! |

||

|

||

|

Finally, here are some simple DO’s and DON’T’s so you have the best chance of winning one of the prizes: |

||

|

||

|

This is an exciting contest and I cannot thank you enough for getting involved! Good luck and If you have any questions, please let me know. |

||

|

||

|

|

||

General Angela Calla 22 Jul

Watch BNN’s video about precautions in case of a mortgage meltdown.

Questions on determining the best mortgage for you and your future? The Angela Calla Mortgage Team is here to help call us at 604-802-3983 or callateam@dominionlending.ca We look forward to helping you.