Another Month, Another Dip In Housing

Statistics released today by the Canadian Real Estate Association (CREA) show home sales edged down in November. National home sales fell 3.3% between October and November, continuing the moderating sales trend that began last February on the precipice of unprecedented monetary policy tightening. Sales are down a whopping 39% from a year ago. The Bank of Canada has hiked their overnight policy rate by 400 bps, from 25 bps to 4.25%, triggering a whopping rise in mortgage rates.

About 60% of all local markets saw lower sales in November, led by Greater Vancouver and the Fraser Valley, Edmonton, the Greater Toronto Area (GTA) and Montreal.

The actual (not seasonally adjusted) number of transactions in November 2022 came in 38.9% below a near-record for that month last year. It stood about 13% below the pre-COVID-19 10-year average for November sales (see chart below).

New Listings

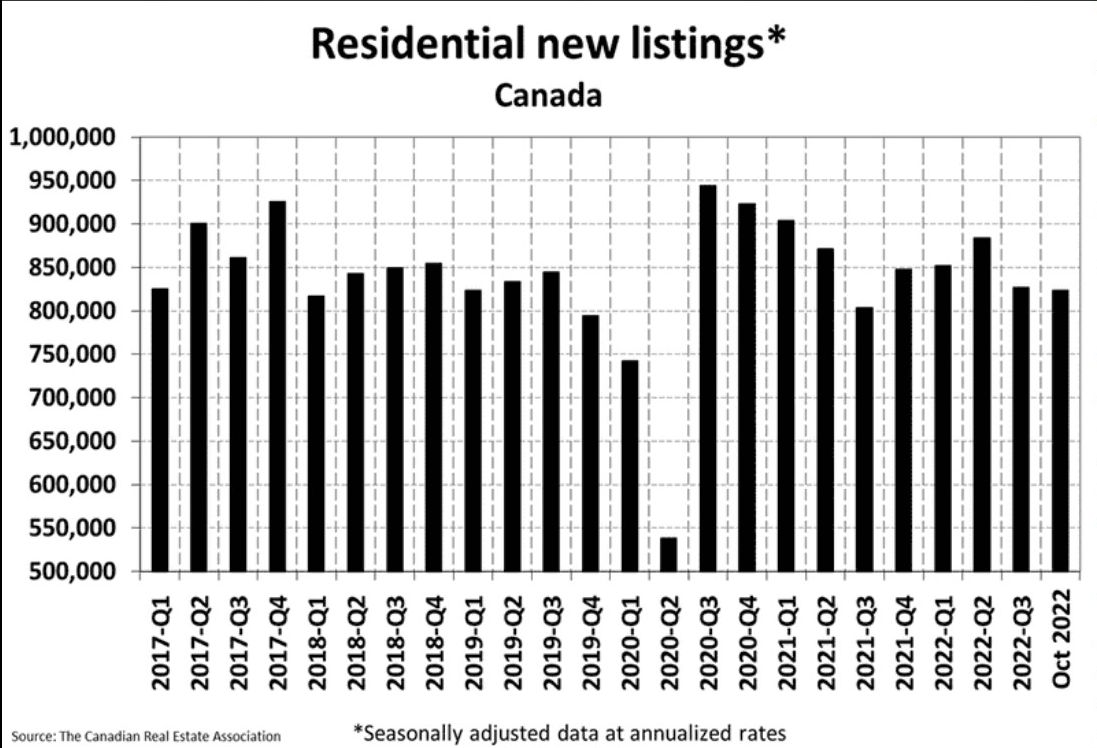

Sellers remain on the sidelines as the number of newly listed homes edged down last month by 1.3%, declining 6.1% from a year ago. Most sellers are waiting for interest rates to fall, either because they expect a rebound in sellers or are unwilling to buy new properties themselves with mortgage rates so high.

While sales have swung wildly, new listing flows have remained relatively steady through the recent turbulence and are very much in line with pre-COVID norms. There’s still not a lot of forced selling, which can exacerbate a price correction.

New listings fell in slightly more than half of the local markets. Among the larger markets in Canada, month-over-month movements in new supply were generally small, the only exception being some more significant declines in the B.C. Lower Mainland and Okanagan regions.

In terms of monthly new supply, the bigger picture is listings are not flooding the market. With the one exception of 2019, November 2022 saw the fewest new listings for that month in 17 years.

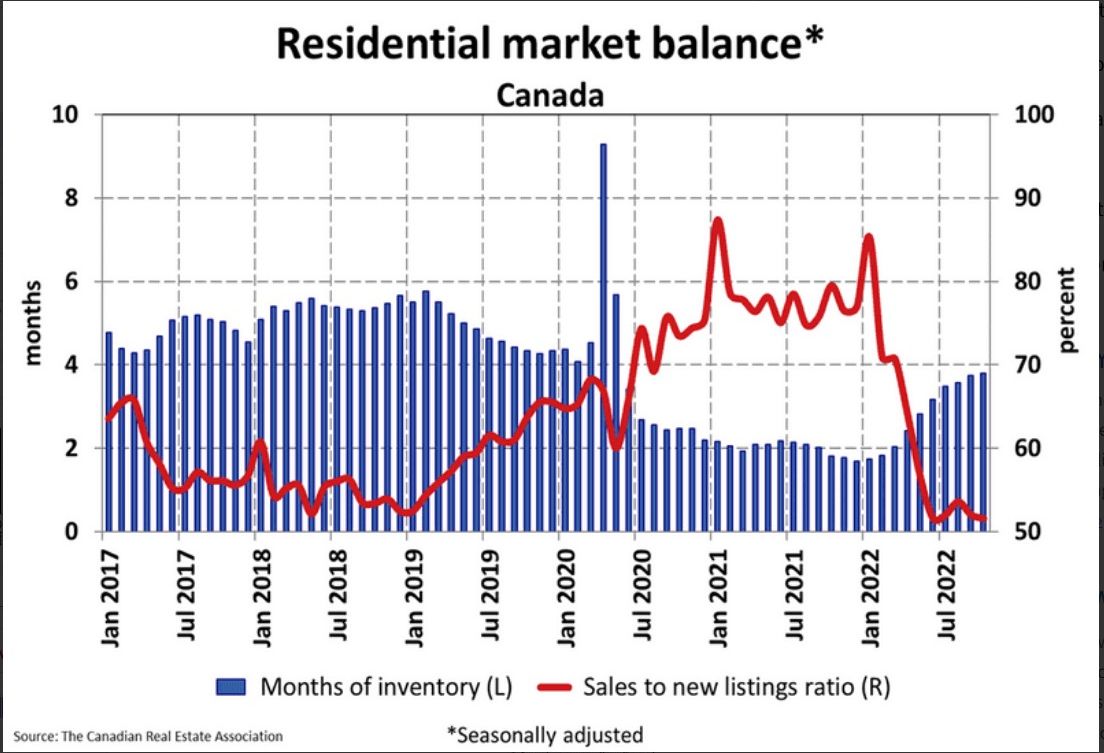

With sales down month-over-month by a little more than new listings in November, the sales-to-new listings ratio fell to 49.9% compared to 50.9% in October. The ratio has remained close to around 50% since May. The long-term average for this measure is 55.1%.

Based on a comparison of the current sales-to-new listings ratio with long-term averages, about 70% of local markets are currently in balanced market territory.

There were 4.2 months of inventory on a national basis at the end of November 2022. This is close to where this measure was in the months leading up to the initial COVID-19 lockdowns and still nearly a full month below its long-term average.

Home Prices

The Aggregate Composite MLS® Home Price Index (HPI) edged down 1.4% month-over-month in November 2022, continuing the trend that began in the spring.

The Aggregate Composite MLS® HPI now sits about 11.5% below its peak level. Breaking that down regionally, the general trend is prices are down somewhat more than they are nationally in Ontario and parts of B.C. and down by less elsewhere. While prices have softened to some degree almost everywhere, Calgary, Regina and Saskatoon stand out as markets where home prices are barely off their peaks at all.

The table below shows the decline in MLS-HPI benchmark home prices in Canada and selected cities since prices peaked in March when the Bank of Canada began hiking interest rates. More details follow in the second table below. The most significant price dips are in the GTA and the GVA, where the price gains were spectacular during the COVID-shutdown.

Bottom Line

OSFI announced this morning that the minimum qualifying rate for uninsured mortgages at federally regulated financial institutions would remain unchanged. They will review Guideline B-20 next month, but don’t hold your breath for an easing of the stress test.

In other news, housing starts were little changed last month at 264,600 annualized units. This is a strong level of new construction; the year-to-date average is roughly 265,000 units. Combined with the record 275,000 new units started last year, we are in line for the most significant two-year wave of housing starts on record. On a per-capita basis, we’re starting 2023 with an unprecedented construction boom despite higher costs, labour shortages and much higher interest rates.

Outlook

The Bank of Canada is likely to raise the policy rate a couple of times by 25 bps in the first half of next year, pausing between rate hikes. They will not cut rates in 2023 even though the economy will post at least a mild contraction.

2024 will be a recovery year but don’t expect the overnight rate to return to the pre-Covid level of 1.75%. Indeed, the new cycle low will likely be more like 2.5% assuming inflation continues to trend downward. Price growth will be much more subdued than during the rocking ten-year period before the pandemic. Still, the underlying fundamentals of rapid population growth, mainly from immigration, bode well for sustained growth going forward.

Angela Calla is an 18-year award-winning woman of influence which sets her apart from the rest. Alongside her team, Angela passionately assists mortgage holders in acquiring the best possible mortgage. Through her presence on “The Mortgage Show” and through her best-selling book “The Mortgage Code“, Angela educates prospective home buyers by providing vital information on mortgages. In light of this, her success awarded her with the 2020Business Leader of the Year Award.

Angela is a frequent go-to source for media and publishers across the country. For media interviews, speaking inquiries, or personal mortgage assistance, please contact Angela at hello@countoncalla.ca or at 604-802-3983.

Click here to view the latest news on our blog.